15 Top Fintech Software Development Companies in 2026 (Vetted on Engineering and Compliance)

Andrew BurakCEO and Founder at Relevant Software

Andrew BurakCEO and Founder at Relevant SoftwareFintech fails differently from other software: a bug in a social app annoys users, but an issue in a payment ledger double‑charges them, corrupts reconciliation, and surfaces in an audit months later. This single difference should guide who builds your financial product and how you evaluate them.

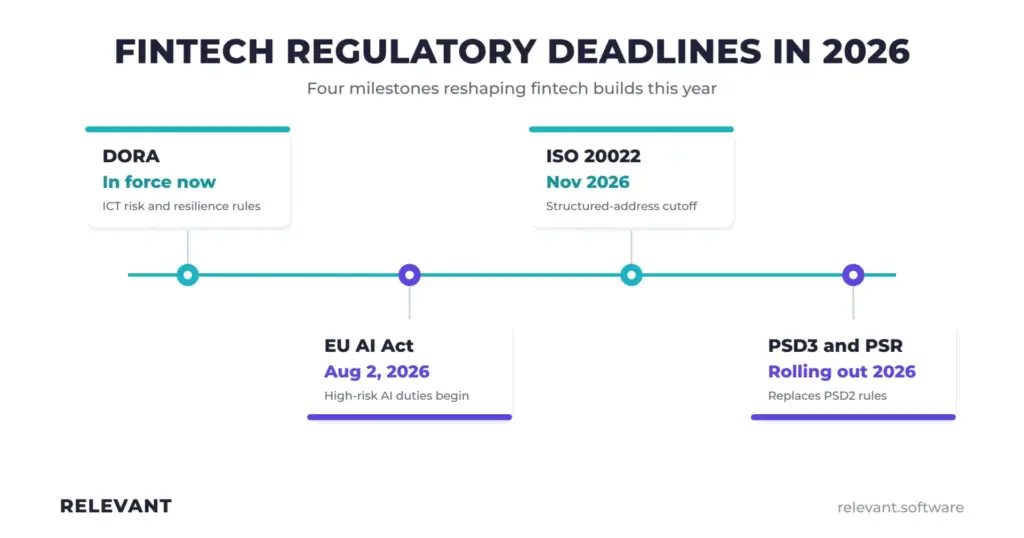

The money behind the market raises the stakes. Fortune Business Insights projects it to reach $460.76 billion in 2026, on the way to $1.76 trillion by 2034. KPMG counted $116 billion of fintech investment in 2025 across 4,719 deals, up from $95.6 billion the year before. Capital is flowing into financial software, and so is regulatory scrutiny. Three deadlines hit in 2026 alone: the EU AI Act and DORA compliance milestone on August 2, the Swift ISO 20022 structured‑address cutoff in November, and the continued rollout of PSD3. Each one changes what “production‑ready” means for a fintech build.

This shortlist takes an engineering‑first view. We looked for verifiable Clutch data, real fintech delivery, and a documented security and compliance posture, not marketing claims. Below, you’ll find the criteria that separate top fintech software development companies from a general software shop, a side‑by‑side comparison of 15 firms, and the regulatory and cost realities that determine whether your project ships on schedule.

TL;DR

- Among the top fintech software development companies in 2026 are Relevant Software, Innowise, Vention, Cleveroad, Itexus, S-PRO, Django Stars, Geniusee, SumatoSoft, Interexy, Orangesoft, 10Clouds, 10Pearls, HES FinTech, and DBB Software. Together, they span boutique specialists to enterprise-scale teams, all with active Clutch profiles and verifiable fintech delivery.

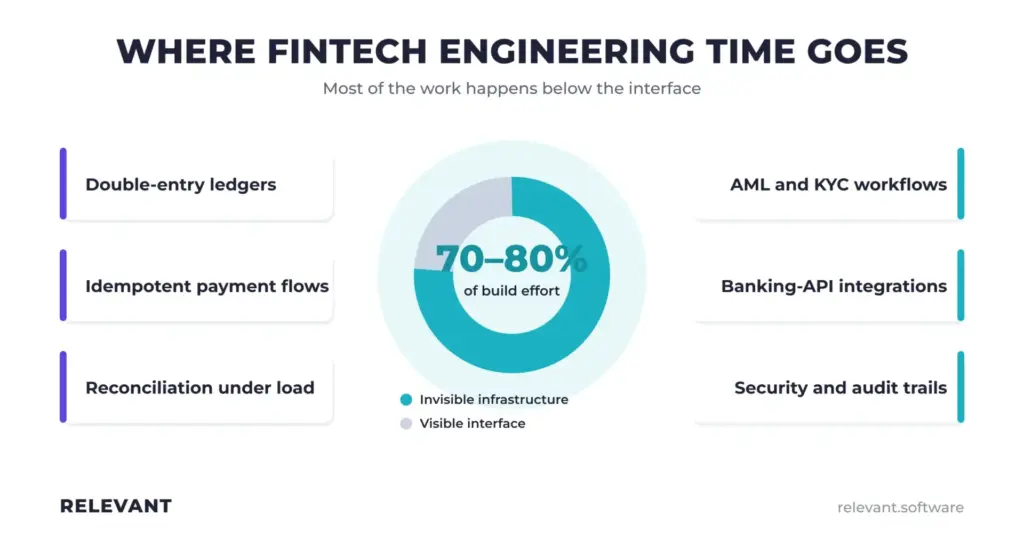

- Fintech software is harder than ordinary software because 70%-80% of engineering time goes into invisible infrastructure: double-entry ledgers, idempotent payment flows, decimal-precision money math, reconciliation under concurrency, and audit trails. If you get this foundation wrong, issues appear under load or in an audit.

- Evaluate partners on engineering: compliance by design (PCI DSS, GDPR, SOC 2 from the first sprint), secure SDLC, financial-grade testing, integration coverage, a senior team that isn’t swapped for juniors after signing, plus clear IP and exit terms.

- Three regulatory deadlines reshape 2026 builds: the EU AI Act and DORA milestone on August 2 (with fines up to 35 million euros or 7% of global turnover), the Swift ISO 20022 structured-address cutoff in November, and the ongoing rollout of PSD3.

- DORA changes vendor selection itself: outsourcing development makes your partner an ICT third-party provider. You stay fully responsible, contracts need Article 30-style clauses (audit rights, subcontracting controls, incident notice, exit support), and you must maintain a Register of Information.

- AI in fintech is now a governance problem. Credit-scoring and insurance-pricing models are high-risk under the AI Act, which means documented data, human-in-the-loop escalation, explainability, and a traceable audit trail.

- Hidden costs add 30%-50% beyond the headline rate: PCI penetration testing runs $12,000–$25,000, post-launch compliance remediation costs 15%-25% of the contract value, and mistakes are expensive (Coinbase settled for $100 million, Monzo was fined £21 million).

- Budget realistically: discovery and prototypes start around $30,000; enterprise fintech builds typically run $150,000 to $1,000,000+; and a senior in-house fintech engineer costs $150,000–$250,000 a year, which is why roughly 70% of companies outsource.

- The fintech market is projected to be $460.76 billion in 2026, with $116 billion invested across 4,719 deals in 2025, so the cost of picking the wrong partner is rising alongside the opportunity.

The 2026 Fintech Engineering Reality

The defining shift in 2026 is the move from pilots to production. AI that lived in proof-of-concept decks last year now runs in live operations. JPMorgan’s AI assistant, Coach, cut advisor research time by about 95% and helped drive roughly $1.5 billion in savings from fraud prevention and efficiency improvements. A CFO survey found 59% of finance functions using AI in 2025, up from 37% in 2023. For builders, the question is how to run it under financial-grade controls.

Embedded finance is turning into infrastructure. Juniper Research expects the global embedded finance market to pass $138 billion in 2026, as payments, lending, and insurance get stitched into non-financial products. Neobank adoption is climbing toward 360 million users worldwide, and 87% of global banks have implemented open banking. Mordor Intelligence puts the AI-in-fintech segment at $30 billion in 2025, with a path to $83.1 billion by 2030.

Underneath this sits a quieter change: data. The Swift ISO 20022 migration ended its cross-border coexistence period on November 22, 2025, and richer structured payment data is now the norm. Institutions that treat the new format as a one-off compliance task stay technically compatible, but commercially behind. Those that build on the structured data win on reconciliation, fraud detection, and product speed. Every serious fintech built in 2026 has to account for this.

Why Fintech Software Is Harder to Build

Most of the work in a fintech product is invisible to the end user. Industry estimates put 70% to 80% of engineering time into the hidden structure: reconciliation, settlement, AML and KYC workflows, integrations, and security. The screens customers see sit on top of a much larger system that has to be correct to the cent. A general software team can ship a polished interface and still get the foundation wrong in ways that only show up under load or in an audit.

A few problems separate fintech engineering from ordinary CRUD applications:

- Money math. Floating-point numbers can’t represent currency reliably. A small rounding error in a ledger grows into a reconciliation gap that auditors eventually find. Robust systems use fixed-precision decimals and a double-entry ledger from day one.

- Idempotency. Networks retry. A payment endpoint without idempotency keys can charge a customer twice for a single request. Getting exactly-once behavior right across distributed services is a core fintech skill.

- Reconciliation under concurrency. Balances have to remain consistent when thousands of transactions hit the same accounts simultaneously. This is where weak architectures break.

- Audit trails. Every state change needs an immutable, queryable record. Regulators and auditors expect to reconstruct who did what, when, and why.

None of this shows up in a portfolio screenshot. It becomes obvious when the partner can talk fluently about ledger design, transaction isolation, and replay safety before you sign anything. A team that treats a banking backend like a generic web app will cost you more in remediation than you ever saved on the rate.

How to Evaluate a Fintech Development Company: An Engineering Checklist

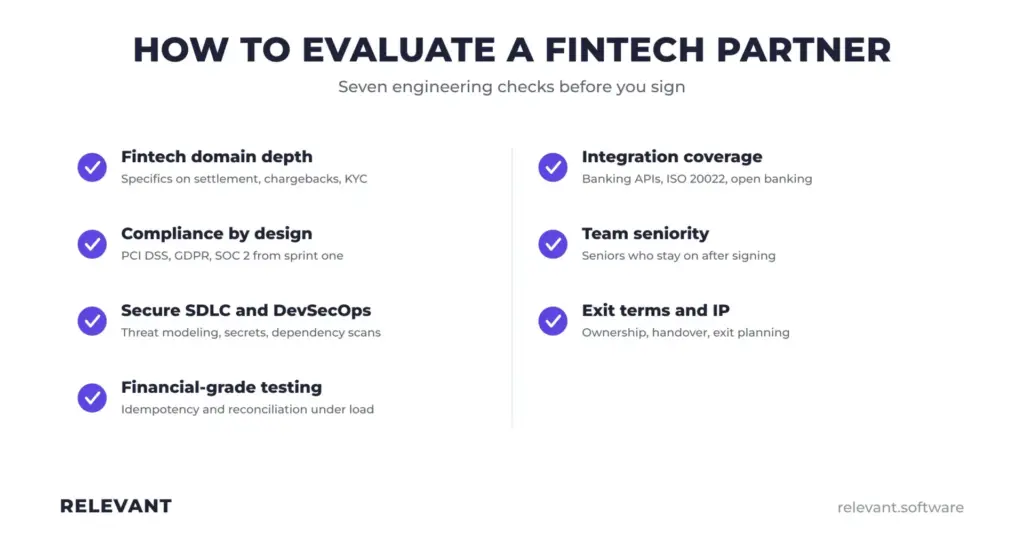

Clutch stars and case-study logos are initial filters. Two firms with identical ratings can differ widely in costs, driven by architectural choices that matter more than hourly rates. Use the checklist below to pressure-test any shortlist.

- Fintech domain depth. Ask for specifics on banking, payments, lending, or wealth, not “financial services” claims. Depth shows up in how they talk about settlement, chargebacks, and KYC.

- Compliance by design. A good partner designs for PCI DSS, GDPR, SOC 2, and the relevant regional rules from the first sprint. Bolting compliance on after launch is the most expensive mistake in fintech delivery.

- Secure SDLC and DevSecOps. Look for threat modeling, secrets management, dependency scanning, and documented secure coding practices. Certifications such as ISO 27001 and SOC 2 Type II are evidence.

- Financial-grade testing. Standard QA budgets don’t cover idempotency edge cases, ledger reconciliation under concurrent load, or decimal-precision regression tests. Make sure these are in scope.

- Integration coverage. Banking APIs, card networks, ISO 20022 messaging, and open banking connections have their own failure modes. Experience here can save months.

- Team composition and seniority. Confirm who writes the code. A senior-weighted team that isn’t swapped out for juniors after signing is worth a premium on a regulated product.

- Engagement flexibility and exit terms. Clarify IP ownership, knowledge transfer, and what happens when the engagement ends. In the EU, exit planning is now a regulatory expectation.

Run every company below through this list in the context of your product. The ranking that follows reflects verifiable credentials, but the right fit still depends on your stage, stack, and regulatory exposure.

The List of the Top Fintech Software Development Companies

The companies below were chosen for proven fintech delivery, active Clutch profiles, a documented security posture, and a mix of sizes from boutique specialists to enterprise-scale teams. The figures are based on publicly available data from company sites and Clutch at the time of writing. Ratings and team sizes change, so confirm current numbers before you engage.

| Company | Founded | Team size | Clutch | Fintech focus |

| Relevant Software | 2013 | 200+ | 4.9 | Core banking, payments, wallets, and onboarding |

| Innowise | 2007 | 1,700+ | 4.9 | Banking, insurance, payments |

| Vention | 2002 | 3,000+ | 4.9 | Banking, lending, insurance |

| Cleveroad | 2011 | 280+ | 4.8 | Neobanking, payments, trading, open banking |

| Itexus | 2013 | 100+ | 4.9 | Digital banking, trading, crypto, RegTech |

| S-PRO | 2014 | 250+ | 4.9 | Banking, crypto, and Web3, wealth |

| Django Stars | 2008 | 100+ | 4.8 | Lending, mortgage, data-heavy backends |

| Geniusee | 2017 | 50-249 | 5.0 | eWallet, banking, lending, trading |

| SumatoSoft | 2012 | 50-249 | 4.9 | Fintech, proptech, custom platforms |

| Interexy | 2017 | 150+ | 4.8 | Web3 wallets, DeFi, AI fintech |

| Orangesoft | 2011 | 50-249 | 4.9 | Mobile-first fintech, payments |

| 10Clouds | 2022 | 200+ | 4.9 | Fintech, blockchain, production AI |

| 10Pearls | 2004 | 1,000+ | 4.9 | Digital payments, embedded finance |

| HES FinTech | 2012 | 50-249 | 5.0 | Lending platforms, credit scoring |

| DBB Software | 2015 | 50-249 | 5.0 | Core banking, KYC and AML, payments |

1. Relevant Software

Relevant is one of the top fintech software development companies on this list, as it pairs proven delivery with deep domain expertise. Founded in 2013, the company has a team of more than 200 engineers, 92% of whom are senior. This mix directly addresses the junior‑substitution risk that undermines many regulated builds.

The track record is documented:

- 246 projects delivered across 13+ years.

- 98% client satisfaction rate.

- 4.9 rating on Clutch with a 9.8 Net Promoter Score.

- 93% on-time delivery rate.

In fintech specifically, Relevant builds the systems where correctness is non-negotiable:

- Core banking systems, payment platforms, and digital wallets.

- Banking-API integration with automated clearing and reconciliation.

- Digital onboarding with KYC and KYB verification.

- Ongoing support that keeps clients aligned with shifting financial regulations.

One of Relevant’s projects, an AI platform for a leading European bank, shows this depth in practice. The client, a century-old bank serving millions of customers in several countries, wanted to turn its transaction data into an edge against digital-first challengers without risking compliance.

Working with CX Design, Relevant built an end-to-end AI platform: predictive models for loans, cards, and deposits; data pipelines processing millions of records daily; secure APIs to core systems; and a GDPR-ready layer with encryption, access controls, and full audit logs. The platform remained 100% GDPR- and PSD2-compliant while cutting analyst workload by 35%, speeding up decision-making by 40%, and delivering insights in 0.8 seconds across more than 650 self-service reports per month.

This maps directly to precise money handling, audit-ready architecture, and compliance designed in from the start. The fit is strongest for technical founders and financial institutions that want a senior, nearshore team with a proven record in regulated products.

If a regulated fintech build is on your roadmap, book a free discovery call with the Relevant team to get a scoped estimate for your product.

2. Innowise

Innowise brings enterprise-scale capacity to fintech work, with more than 1,700 engineers on staff and a wider in-house bench of thousands, built up since 2007. It holds a 4.9 Clutch rating across more than 70 reviews and delivers under ISO 9001, ISO 13485, and ISO 27001 certifications, with a reported 1,600+ projects shipped to clients in 60+ countries.

In financial software, the company works across banking, insurance, and payments, and its case library covers fraud detection, AML transaction monitoring, KYC software, payment hubs, open banking platforms, and crypto exchanges. Regional business teams sit across North America, the DACH region, the UK, the Nordics, and the Middle East, so engagements can account for local regulatory and business context. Roughly 93% of its clients stay engaged beyond a year.

Its fintech capabilities span:

- Banking platforms, payment systems, and lending products.

- Fraud detection, AML monitoring, and KYC and KYB workflows.

- Crypto exchanges and blockchain integration. AI, data engineering, and cloud and DevOps support.

Best for enterprises that need to stand up large, cross-functional teams quickly, whether for a greenfield build or a legacy modernization, and that value regional coverage across the EU, UK, and US.

3. Vention

Vention, formerly iTechArt, has operated since 2002 and employs more than 3,000 engineers across 10+ delivery locations. A 4.9 Clutch rating reflects a consistent record in regulated financial software, and the scale is the point: where a boutique would need months to hire, Vention can staff several concurrent workstreams from an existing bench.

The company builds across banking, lending, and insurance, and is a common choice for established players modernizing legacy payment infrastructure, where the work demands both domain understanding and raw capacity. Engagements run as dedicated teams that scale up or down as scope shifts, which suits multi-quarter programs with changing requirements rather than fixed, one-off projects.

Its fintech strengths include:

- Banking, lending, and insurance platforms.

- Legacy payment infrastructure modernization.

- Dedicated teams that flex with scope.

- Full-cycle product engineering across web and mobile.

Best for large fintechs and established institutions whose primary constraint is engineering capacity rather than domain knowledge, and who need a partner that can build a team quickly and sustain it over a long-term roadmap. A startup that wants a small, senior-only boutique may find the scale more than it needs.

4. Cleveroad

Cleveroad earned a place among Clutch’s top five US custom software developers in early 2026, a ranking driven by active client feedback. The company has completed 250+ projects since 2011. The team consists of 280+ in-house engineers and can draw on a 2,100-strong specialist external network to scale niche skills. It holds ISO 9001 and ISO 27001 certifications, with delivery aligned to PCI DSS, SOC 2, GDPR, and PIPEDA.

Its fintech portfolio is broad: neobanking and digital banking, payment systems, trading platforms, insurance automation, micro-investment apps, and open banking. The company emphasizes secure, compliant architecture and clean integrations, and it has shipped products aligned with regional frameworks such as Saudi Arabia’s SAMA rules.

Its fintech work spans:

- Neobanking, digital banking, and payments.

- Trading platforms and insurance automation.

- Micro-investment and open banking products.

- Cloud, DevOps, and AI and data science support.

Best for regulated products that need certified processes and a documented security posture from day one, with the flexibility to scale specialized skills on demand. The combined in-house and network model fits teams that want a stable core supplemented by niche expertise when a project calls for it.

5. Itexus

Itexus has built financial software exclusively since 2013, and this focus shows in the numbers: more than 300 fintech projects delivered for clients across the US, Europe, and the MENA region, with a dedicated fintech division and the promise to ship MVPs in under 4 months. A 4.9 Clutch rating spans more than 40 reviews, and delivery follows SOC 2, PCI DSS, and ISO 27001 standards.

The portfolio is deep for a mid-sized firm. The team has built PCI DSS-compliant cryptocurrency wallets, white-label banking platforms, and digital onboarding with automated KYC and KYB for a large credit union, and it works across digital banking, stock trading, investment and risk scoring, insurance, RegTech, and AI-powered finance assistants. Because the company focuses solely on fintech, it brings domain knowledge and compliance expertise into each build.

Its domain coverage includes:

- Digital banking, stock trading, and investment management.

- Crypto wallets and white-label banking platforms.

- Digital lending, RegTech, and insurance.

- AI finance assistants and financial data integrations.

Best for founders who want a partner that lives entirely in the financial domain, especially for compliance-heavy products that need to reach the market fast. A company whose roadmap may later expand well beyond finance might find the specialization narrower than it needs.

6. S-PRO

Blockchain and digital assets are where S-PRO stands out, built on a foundation of core banking and wealth work it has delivered since 2014. The roughly 250-person team holds a 4.9 Clutch rating across more than 40 reviews, and its client roster includes a global digital-asset banking group with Swiss and Singapore heritage.

The company builds custom fintech for banks that modernizes operations and simplifies compliance, alongside crypto and Web3 products that lean on its blockchain expertise. Its wealth and investment tooling covers portfolio tracking, risk analysis, automated reporting, and real-time insights, and it brings additional depth from healthcare, energy, and real estate, which helps with products that touch insurance or embedded finance.

Its core strengths:

- Banking platforms and modernization for financial institutions.

- Crypto, Web3, and tokenization products.

- Wealth and investment tools with analytics and reporting.

- Risk analysis and automated financial workflows.

Best for products where decentralized infrastructure, tokenization, or crypto rails sit at the center of the build, and for banks that want a modernization partner equally comfortable with legacy systems and emerging digital-asset rails.

7. Django Stars

Python and Django are the core of Django Stars, a focus the company has maintained since 2008 as it builds fintech products for the US, UK, and Swiss markets. The 100+ team holds ISO 9001, ISO 14001, and ISO 27001 certifications and has a 4.8 Clutch rating.

The deliberate technology focus pays off in data-intensive financial backends, where Python’s data and machine learning ecosystem is an advantage. The company’s lending and mortgage work is its calling card: it built the MVP for Molo Finance, a digital mortgage broker, and worked on the MoneyPark digital mortgage platform, both in markets with demanding regulatory expectations.

Where it delivers:

- Data-intensive fintech backends.

- Lending and digital mortgage products, including Molo Finance and MoneyPark.

- API design and scalable backend architecture.

- Long-term product development and maintenance.

Best for backend-heavy, data-driven products that benefit from deep Python and Django expertise, particularly in lending, mortgage, and other data-rich financial domains. Teams that need a broad multi-stack generalist may prefer a larger, less specialized shop.

8. Geniusee

Geniusee carries a 5.0 Clutch rating across 65 reviews and has paired the delivery quality with competitive rates since 2017. The company builds fintech products with cloud-native engineering and a clear focus on getting early-stage products to market without cutting corners on financial rigor.

Its fintech work spans eWallet, digital banking, lending, and trading solutions, and the team combines product design with full-cycle development, enabling a founder to move from concept to a shippable product with a single partner. For startups, the appeal is a top-rated team at rates that leave more runway, without the bureaucracy that can come with much larger vendors.

Its work covers:

- eWallet and digital banking solutions.

- Lending platforms and trading tools.

- Product design and full-cycle development.

- Cloud architecture and scalable infrastructure.

Best for startups that want financial-grade rigor on early-stage builds without enterprise pricing, particularly where speed, a clean delivery record, and design-led product work matter as much as raw engineering.

9. SumatoSoft

SumatoSoft works as an embedded technology department. This is the model it has refined since 2012. The approach reduces handoff friction that slows platform iteration by integrating with a client’s processes. A 4.9 Clutch rating is based on 25 verified reviews. The company has delivered production systems to clients such as Toyota and Beiersdorf.

Its work covers fintech and proptech alongside healthtech and other data-heavy domains, and it keeps product design and software engineering under one team, which holds design and build in step. For platform products that iterate continuously, this single-team structure is an advantage over a vendor that passes deliverables back and forth across a wall.

The capabilities include:

- Custom fintech and proptech platforms.

- Web and mobile engineering.

- Product design and UX research.

- AI and cloud solutions.

Best for product teams that want engineering to feel like an extension of their own staff, with consistent delivery, transparent project management, and tight design-to-build alignment.

10. Interexy

Blockchain-native and AI-first products are Interexy’s home ground. Working from a Miami base since 2017, the team of roughly 150 pairs deep blockchain knowledge with AI and machine learning. Reviewers flag predictable sprints, daily syncs, and an 87% client retention rate, which carry weight in fintech, where systems that underperform are quickly replaced.

The company builds Web3 wallets, DeFi platforms, crypto payment apps, and AI-powered financial products, and it has experience with regulated EMI and PI builds, which matters for teams launching licensed money products. Its sweet spot is the project where both blockchain and AI are hard requirements.

Its focus areas:

- Web3 wallets and crypto payment apps.

- DeFi platforms and tokenized products.

- AI-powered financial tools and lending platforms with automated tracking.

- Regulated EMI and PI product builds.

Best for founders launching digital-asset or AI-first products who need to reach the market quickly without building core infrastructure from scratch, and who want a partner fluent in both blockchain and AI.

11. Orangesoft

Mobile-first development defines Orangesoft, a Clutch Global Leader that has shipped more than 250 projects since 2011. The team carries a 4.9 Clutch rating and works across fintech, healthcare, and IoT, with particular depth in native iOS and Android engineering and cross-platform delivery.

For consumer fintech, where the mobile experience is the product, such a focus is an advantage. Orangesoft builds payment apps, digital wallets, and other financial products with attention to the polish and performance that drive retention, alongside the secure logic these products require. The company suits teams that have validated a concept and need a well-engineered mobile build.

What it builds:

- Consumer fintech apps and payment products.

- Native iOS, Android, and cross-platform front ends.

- UX-led mobile delivery.

- Backend support for mobile financial logic.

Best for products where the mobile experience is the core of the offering and needs to sit atop solid, secure financial logic, particularly consumer-facing fintechs aiming for strong engagement and retention.

12. 10Clouds

10Clouds pairs product design with production AI, shipping live systems for banks, insurers, and fintechs. The team of 200 has a 4.9 Clutch rating and has earned growth recognition from the Financial Times and Deloitte, with a tech stack spanning React, Node.js, Python, Elixir, and Solidity.

The company has moved aggressively into agentic AI for financial operations, including credit automation and agentic commerce, while keeping product and UX design in-house alongside engineering. This design-and-build combination suits products where the experience and the AI must be right, not merely functional, and its blockchain heritage rounds out a profile aimed at modern, AI-heavy financial products.

Its strengths:

- Fintech and blockchain product development.

- Credit automation and agentic AI workflows.

- Product and UX design alongside engineering.

- DevOps and MLOps support.

Best for products that need strong design together with AI and blockchain capability rather than raw staff augmentation, especially teams putting AI into production inside a regulated financial environment.

13. 10Pearls

10Pearls is an enterprise-scale partner operating since 2004, with more than 1,000 people across the US, UK, and Latin America, and a 4.9 Clutch rating. It focuses on financial services, digital payments, and embedded finance. Moreover, its work has drawn recognition from Gartner and Forrester.

The company’s fintech credentials are specific: it has built and modernized platforms for providers like BillGO, Corcentric, and Galileo. The company also pairs custom development with strong data, machine-learning, and AI capabilities. A global delivery footprint across multiple time zones supports near-continuous productivity, which suits large programs on aggressive timelines. For established institutions, the draw is breadth: strategy, engineering, data, and modernization under one roof.

Its areas of focus:

- Digital payments and embedded finance.

- Data, machine learning, and AI for financial products.

- Digital banking and lending applications.

- Modernization for established institutions.

Best for established financial institutions and scale-ups that need broad engineering capacity, real data, and AI depth, and round-the-clock delivery across time zones.

14. HES FinTech

Lending is HES FinTech’s entire focus, so the specialization runs deep: its platforms are used by more than 130 companies across the UK, US, Canada, Australia, and the MENA region. The team holds a 5.0 Clutch rating and builds lending infrastructure for banks, alternative lenders, and fintechs.

Its products cover the full lending lifecycle, from loan origination and loan management systems to AI-powered credit scoring and automated decisioning, with compliance and reporting automation built in. Because the company has solved the same hard problems across consumer and commercial lending many times over, it brings proven patterns to a domain where edge cases and regulatory detail can sink a generic build.

What it delivers:

- Loan origination systems and loan management systems.

- AI-powered credit scoring and automated decisioning.

- Compliance and reporting automation for lending.

- Consumer and commercial lending platforms.

Best for lending businesses that want a proven platform depth and a level of domain focus that a generalist shop can’t easily match. Companies building outside lending will find the specialization too narrow.

15. DBB Software

A compliance-first approach defines DBB Software, which has built fintech products since 2015 and earned a spot on the 2025 Clutch 1000 list, with a 5.0 rating. The company works with startups and growth-stage companies that need regulated features built correctly.

Its work centers on the parts of a financial product that carry the most risk: core banking components and ledgers, KYC and AML workflows, and payment systems and integrations. The emphasis on secure, audit-ready architecture from the outset is the right instinct for early teams, since fixing compliance and security after launch is the most expensive path in fintech. For a younger company, such discipline can be the difference between passing an enterprise security review and stalling on one.

Its build focus:

- Core banking components and ledgers.

- KYC and AML workflows.

- Payment systems and integrations.

- Secure, audit-ready architecture.

Best for early-stage and growth fintechs that want a security-aware partner to build regulated features correctly the first time.

The Regulatory Stack Fintech Builds Must Satisfy in 2026

In 2026, compliance is architecture you design from the first commit, and it increasingly decides whether you can close deals, raise funding, and partner with banks. The stack below is the baseline for most fintech products that touch the EU, UK, or US.

- DORA. The EU Digital Operational Resilience Act has been in effect since January 17, 2025, and in 2026, it moves from guidance to enforcement. It sets direct requirements for ICT risk management, resilience testing, incident reporting, and third-party oversight across almost all regulated financial entities in the EU.

- EU AI Act. High-risk obligations for fintechs are due on August 2, 2026. AI used for credit scoring, insurance pricing, or biometric verification is high-risk, which triggers requirements for documentation, human oversight, and explainability. Penalties can reach 35 million euros or 7% of global turnover. For many fintechs, this is as consequential as GDPR.

- PSD3 and PSR. The third Payment Services Directive and the new Payment Services Regulation replace PSD2, tightening rules on fraud, strong customer authentication, and open banking access.

- ISO 20022. The cross-border coexistence period ended on November 22, 2025. The next hard deadline is November 2026, when unstructured addresses will be rejected and only structured or hybrid formats will pass, and MT101 messages will retire in favor of pain.001. Payment systems that still rely on free-text fields will face rejected transactions and rising operational friction.

- PCI DSS, GDPR, and AML. Card data handling, personal data protection, and anti-money-laundering rules remain the backbone, now reinforced by AMLD6 and the new EU anti-money-laundering authority.

If your development partner treats these regulations as a launch-day checklist, you end up with technical debt. A company that designs for them from the start builds audit-ready systems that move faster through bank and investor diligence.

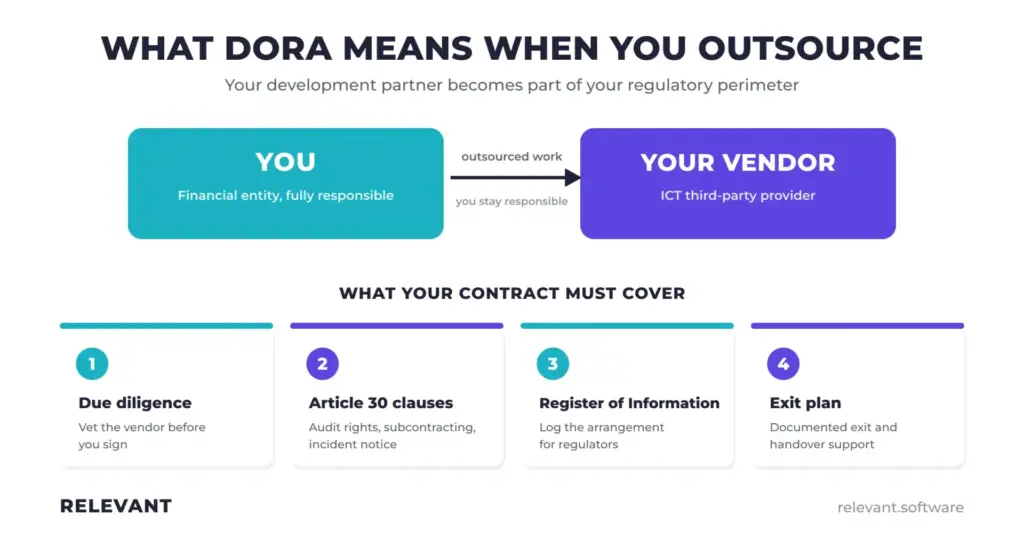

What DORA Means When You Outsource Fintech Development

This is the part most shortlists skip, and it changes how EU-facing fintechs should choose a development partner. Under DORA, once you outsource software development, your vendor becomes an ICT third-party provider with specific obligations.

You stay fully responsible for compliance. A provider’s certifications help, but don’t replace your own due diligence. You still need to assess the vendor, maintain your own register, and ensure the contract meets DORA. Articles 28-30 require pre-contract due diligence, mandatory clauses, concentration-risk analysis, and a documented exit plan. For critical or important functions, contracts must add audit rights, controls on subcontracting, incident notification, and exit support.

EBA outsourcing registers suggest over 60% of critical functions in large EU banks depend on third-party ICT services. In November 2025, regulators named 19 critical third-party providers for direct oversight, and the first Register of Information submissions in early 2026 became a supervisory test.

For buyers, the point is that a partner that knows it sits inside your regulatory perimeter is worth more than one that doesn’t. Ask if they can support Article 30 clauses, provide evidence for your Register of Information, and help with exit planning. A partner that can do this removes risks that a cheaper, compliance-naive vendor pushes back onto you.

AI and Agentic Systems in Fintech: Capability vs. Governance

The agentic AI story in 2026 is about governance. The capability is real and in production: autonomous agents now triage loan applications, run reconciliation, monitor for fraud, and resolve a large share of retail-banking inquiries on first contact. AI coding assistants can increase developer productivity by up to 40%. The challenge is to run these systems under the controls required for a regulated financial product.

Three governance problems separate teams that can deploy AI in fintech from firms that only demo it:

- High-risk classification. Under the EU AI Act, credit scoring and insurance pricing models are high-risk. This means documented training data, human oversight, and the ability to explain a decision to a regulator or a rejected applicant. A black-box model that can’t justify a denial is a liability.

- Human-in-the-loop design. Agents need clear escalation paths. The key question is where the agent acts on its own, where it pauses for a human, and how that boundary is enforced and logged.

- Traceability and grounding. Financial advice and decisions need an audit trail back to the source data. Retrieval-augmented generation over current regulatory and product documents reduces hallucinations, but only if retrieval and logging are built correctly.

A partner that can talk through model governance, explainability, and escalation design is operating at the level fintech now needs.

The Hidden Costs of Fintech Development

The cheapest bid doesn’t mean the cheapest project. In fintech, hidden costs add 30% to 50% to the headline rate, mostly from compliance and financial-grade quality that low bids skip.

A few cost drivers show up again and again:

- Security testing. PCI DSS penetration testing alone runs about $12,000 to $25,000. Add QSA scoping, remediation, and the full review cycle, and you add 8 to 12 weeks.

- Compliance remediation after delivery. Fixing a regulatory finding 6 to 18 months after a project closes costs 15% to 25% of the original contract value. Designing a compliant architecture during development costs a similar 15% to 25% premium, but you pay it once and avoid the rework.

- The invisible backend. With 70% to 80% of engineering time going into reconciliation, settlements, compliance workflows, and integrations, a quote that looks cheap underscopes the part of the system that carries the risk.

The downside of getting this wrong is tangible. For example, Coinbase agreed to a $100 million settlement in 2023 over compliance failures, and Monzo was fined £21 million in 2024 after its internal controls couldn’t keep pace with growth.

On the talent side, retaining a senior fintech engineer in the US or UK costs $150,000 to $250,000 a year, which is why many companies outsource. The financial services outsourcing market is projected to grow from $181.56 billion in 2025 to $342.19 billion by 2035, with about 70% of companies citing cost reduction as the primary driver. Done well, outsourcing also shortens time-to-market by roughly 4 to 6 months compared with building an equivalent in-house team.

Read a fintech quote with one question in mind: what did they leave out? A higher bid that includes security testing, compliance architecture, and proper reconciliation logic results in a lower total cost.

Why Fintech Projects Fail and How to De-Risk Yours

Most unsuccessful fintech builds fail on the foundation, and the reasons are predictable enough to design around.

- Money-handling defects. An idempotency failure in a payment flow results in double-charging customers. A floating-point error in a ledger grows into a reconciliation gap that an auditor eventually finds. Both are preventable with the right architecture and testing, but once they reach production, they are expensive.

- Deferred security. “We’ll fix security after the seed round” is a common and costly decision. By the time enterprise partners and regulators get involved, they expect clear security policies and architecture already in place. A failed SOC 2 audit can stall enterprise deals and trigger 6 to 9 months of remediation and re-audit.

- Scoping mistakes. SOC 2 is a flexible framework. Teams that scope it poorly pay the price in unnecessary costs, extended timelines, and failed audits. A SOC 2 Type II report typically takes 10 to 14 months for a fintech with a reasonable baseline, so it has to be planned.

- Underestimating the invisible system. Teams that budget for the interface but not the ledger, integrations, and compliance layer run out of runway before the product is truly production-ready.

You de-risk a fintech by building the same way every time: choose a partner who designs for compliance and correctness from the first sprint, tests the money paths as rigorously as the features, and treats security as architecture. The cost of skipping it shows up later, larger, and at the worst possible moment.

How Relevant Builds Fintech Products

The earlier profile covered Relevant’s track record. What matters at the close of this guide is how the company works, because in fintech, process is what separates a clean launch from a stalled audit. Relevant runs an engineering-led, AI-accelerated process.

Discovery that de-risks before the budget

Relevant’s AI product discovery compresses the usual 4-8 weeks of scoping into 2-3 weeks and ends with a PRD, an architecture blueprint, a phased budget, and a working prototype. Compliance constraints such as GDPR and SOC 2 are mapped in the first week, while tricky integrations are prototyped and stress‑tested for feasibility before any budget is committed. This keeps fintech projects out of expensive mid‑build surprises.

AI built for production

Through agentic engineering, Relevant develops AI agents that run inside enterprise security boundaries. Each deployment includes:

- Isolated, containerized environments with scoped access and full audit logging.

- Clear decision boundaries: what the agent does on its own, what escalates to a human, and what never gets automated.

- Monitoring, output validation, and rollback if an agent exceeds its limits.

Coverage across the AI lifecycle

The same rigor applies to the messier parts of a build. Each of the offers below solves a version of the same fintech problem: getting from something that looks finished to something that survives load, audit, and regulation:

- AI-driven legacy modernization for institutions running on old core systems.

- AI prototype to production for teams stuck between a working demo and a shippable product.

If this approach fits what you’re building, reach out to Relevant to walk through your idea and get a phased roadmap before you commit to a budget.

Conclusion

Choosing a fintech software development company in 2026 is less about portfolios and hourly rates and more about engineering depth, compliance posture, and verifiable delivery. The market is large and growing, the regulatory bar is rising across several fronts at once, so treating financial software like an ordinary one shows up in remediation delays, failed audits, and lost deals.

The 15 companies in this guide all bring fintech credentials and active Clutch records. The right fit depends on your stage, stack, and regulatory exposure. Use the engineering checklist to pressure-test any shortlist, weigh the hidden costs honestly, and favor partners who design for compliance and correctness.

If you want a senior, fintech-focused team with a proven delivery record, talk to Relevant Software about your project.