Changing the Way We Pay: Top 8 Open Banking Payment Solutions

Andrew BurakCEO and Founder at Relevant Software

Andrew BurakCEO and Founder at Relevant SoftwareOpen banking has revolutionized the financial services industry by introducing a brand new way to manage finances. It allows customers to control their data better and take advantage of a new generation of financial products while turning traditional offline banks into feature-rich service platforms.

At Relevant, we build fintech software, so we track this space closely. Below, we explain how open banking works and walk through eight payment solutions worth knowing.

What is open banking, and how does it change the payment landscape?

Open banking is a practice that allows licensed third-party providers (TPPs) to access customer banking data through application programming interfaces (APIs). A bank can share a customer’s data only if the customer provides consent to such actions. Customers can also control what types of data can be accessed by a TPP and for how long.

How open banking works

In general, TPPs interact with banks on behalf of bank customers to provide the following services:

- Account Information Services (AIS)—for displaying and consolidating information such as balance and transaction history from a customer’s bank accounts.

- Payment Initiation Services (PIS)—for enabling online payments without the need to insert credit card details manually.

To make things clearer, consider the example of a money manager app. Without open banking, the app user has to interact with every bank they have an account with directly (e.g., by logging into the account and copying over the required information) and then insert the relevant data into the app.

With open banking, things get much easier. The user just needs to give the TPP permission to access their bank data. The TPP then interacts with all banks via open banking APIs, retrieving information from all the user’s accounts on their behalf. As a result, the user can see their consolidated transaction history, account balances, and spending in a few clicks.

Open banking payments are based on similar logic. When merchants cooperate with PIS providers, shoppers don’t need to enter personal card details manually to pay for a service or product online. They can just click on a payment link or scan a QR code on a merchant’s website, connect to their bank app, and confirm payment. This way, a merchant doesn’t get access to the customer’s bank information.

The impact of open banking on the finance industry

Open banking has moved from a regulatory concept to a structural shift in how financial services operate. Adoption accelerated during the pandemic, and since then, the model has continued to expand across regions, increasing competition and lowering barriers for fintech innovation. Europe remains the most mature market, but similar frameworks now operate or are emerging in the UK, Australia, Brazil, and parts of Asia.

Growth data reflects that momentum. Industry forecasts show global open banking users growing at a compound annual growth rate of nearly 50% in the early 2020s, with Europe leading adoption. In the UK alone, open banking adoption has grown into millions of active consumers and businesses, sharing account data with regulated third parties to support payments, lending, and personal finance tools.

The benefits extend beyond customers. Open banking forces banks to modernize legacy platforms and expose internal data through APIs, which unlocks operational and product innovation. An Economist Intelligence Unit survey conducted for Temenos found that 45% of banking executives aim to turn their institutions into digital ecosystems, while 29% already include open banking in their innovation strategy. This shows that many banks now view open banking as a catalyst for core transformation rather than a compliance exercise.

Because APIs are accessible to both banks and fintech providers, open banking enables new products, faster partnerships, and deeper customer relationships across the financial ecosystem. Below, we examine the specific advantages this model delivers.

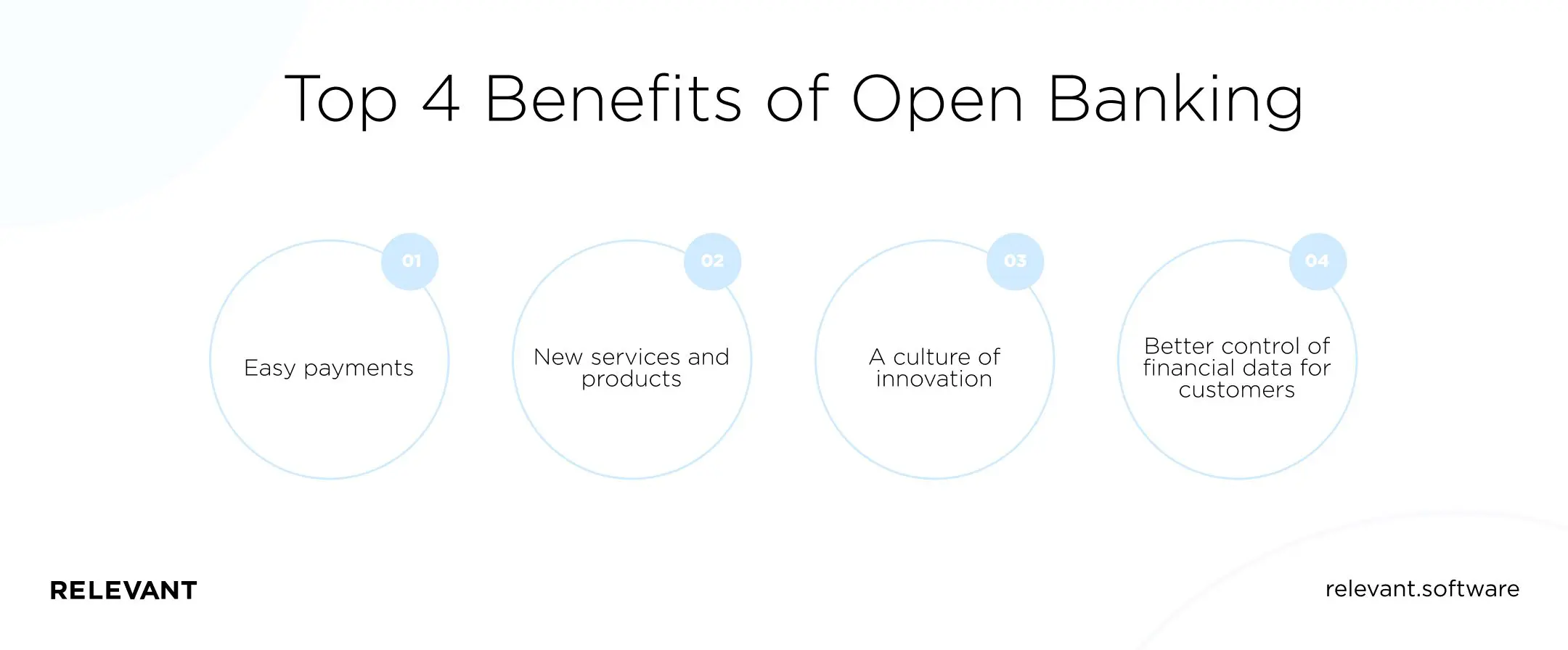

Key benefits of open banking

Open banking has the potential to revitalize the financial sector with a range of benefits for customers, banks, and businesses:

- Easy payments. Using open banking payment services, customers can make payments straight from their bank account, without entering card details. All they need to do is perform one- or two-step authentication through a banking app or website and confirm the payment.

- New services and products. Open banking opens up a lot of new possibilities and potential for product innovation. For consumers, this means more opportunities (think of open banking loans) and easier financial operations, while businesses get access to new markets.

- A culture of innovation. Open banking encourages banks to upgrade their digital infrastructure so that they can securely share customer data. What’s more, modern payment technology helps banks to better structure their data and improve its internal use.

- Better control of financial data for customers. With traditional banking, a customer’s control over their account was limited to what their banking app or website offered. Open banking gives customers broader opportunities for money management and better control over their financial data.

Now that we’ve covered what open banking is, how it’s changing the industry, and what benefits it brings to the table, let’s look at some of the most promising open banking payment solutions on the market today.

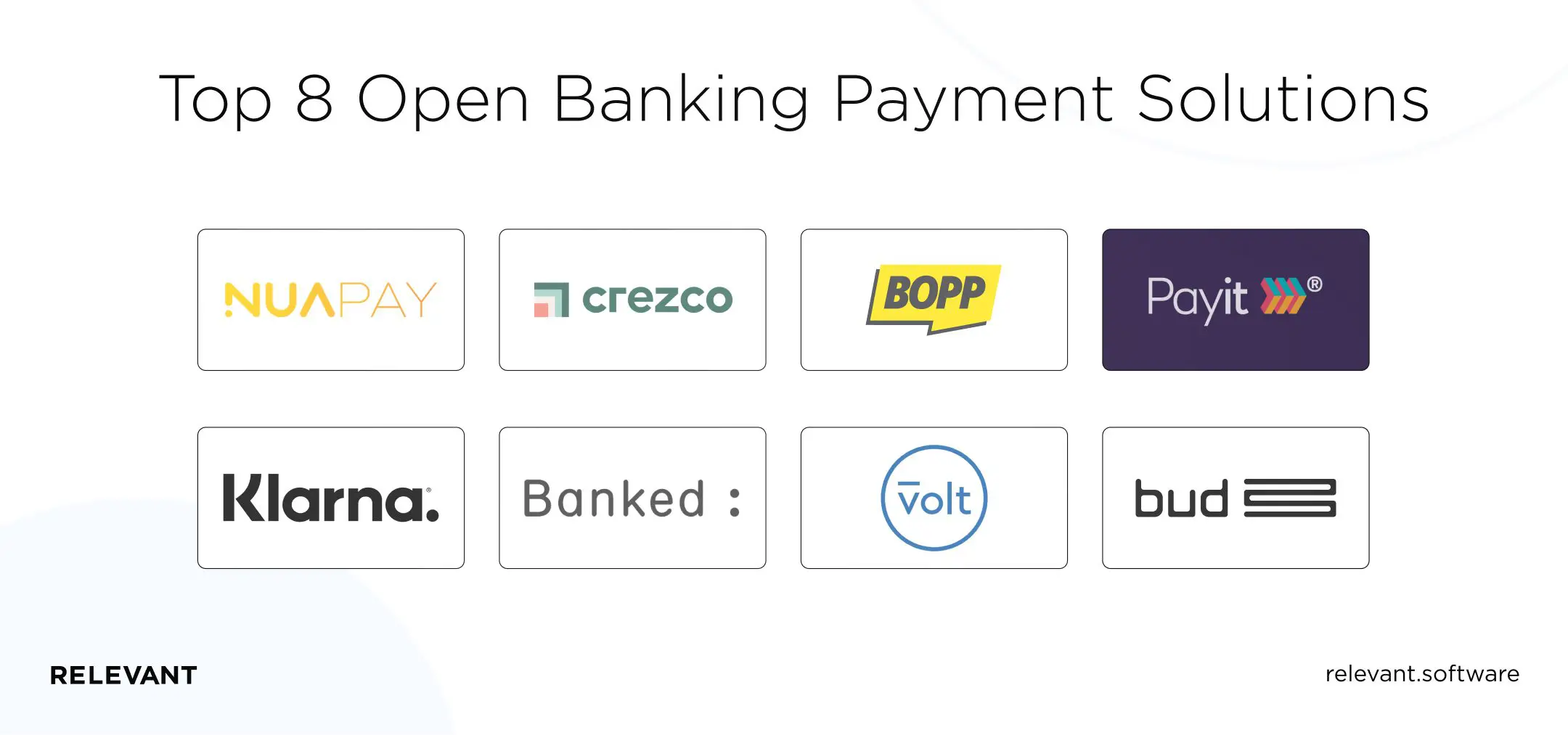

Top 8 open banking payment solutions

According to Open Banking Limited’s Impact Report 7, UK open banking momentum continues to accelerate: 31 million open banking payments were made in March 2025, while active users reached 13.3 million, up 40% year on year. Open banking payments also grew at around 70% year-on-year, indicating that pay-by-bank and recurring payment use cases have moved into the mainstream.

With adoption at this pace, it is no surprise that the online payments market has a clear group of innovators who build products around open banking rails. Here are some notable examples.

1. Nuapay

Nuapay is an Irish open banking pioneer that aims to simplify the management of online payments. Nuapay offers fully integrated settlement services by connecting its customers with thousands of banks across 34 countries. The payment environment has also received industry awards such as Best Online Payments Solution–Merchant in 2020 and the Best Use of Open Banking in the Merchant Payments Ecosystem in 2021.

2. Crezco

Crezco sounds like a dream come true for its absence of processing fees. It’s an open banking payment solution that provides UK-based businesses with a fast, secure, and cost-effective alternative to existing card payment schemes. As well as streamlining online payments, Crezco offers secure and contactless bank transfers: customers only need to scan a QR code and confirm payment. Crezco works with all major UK and European banks.

3. BOPP

The brainchild of London-based fintech Agitate, BOPP uses open banking to remove the need for cards and facilitate immediate, secure payments between bank accounts. It has a quick sign-up process and an easy dashboard for business use and supports fast QR payments. BOPP is entirely free for personal use, while for businesses, it takes a flat monthly fee of £10 for all transactions. BOPP also offers an optional mobile payment solution for consumers.

4. Payit

Payit is one of the leading payment initiation services in the UK by transaction volume. The service is provided by NatWest bank, but its customers don’t need a NatWest account to be able to use it. Since its launch, Payit has processed over 100,000 transactions totaling over £15 million. What makes it stand out from the crowd is its seamless refund system that doesn’t require merchants to know or store customer account information.

5. Klarna

Klarna is one of the best online payment services. It’s best known as “buy now pay later” software, which offers shoppers interest-free financing on retail purchases over a series of installments. It has over 200,000 retail partners, including giants like Samsung, Nike, ASOS, H&M, IKEA, and AliExpress.

Klarna’s open banking platform is just one of its services. Klarna APIs allow businesses to create fintech products ranging from expense-splitting apps to robo-advisors.

What’s more, with Klarna’s white-label solution, PSD2-licensed third-party providers can request and receive bank data. But to integrate the Klarna API into their service, they usually need to hire a development team.

6. Banked

Banked is a London-based open banking startup that enables account-to-account payments at checkout. It allows merchants to offer a direct payment option that bypasses entering credit card details: all customers need to do is go through the authentication process and proceed with payment. Banked works best for small companies where high processing payment fees can negatively influence business since it charges only 0.1% to process payments instead of the 1-4% charge typically seen across the market.

7. Volt

Volt’s open payments gateway raised $23.5 million in a Series A funding round and now connects over 5,000 banks across the UK and EU in a market-leading payment grid. It offers secure payment solutions for customers and helps merchants reduce the cost and complexity of point-of-sale transactions.

8. Bud

Bud is a UK startup that aims to connect customers to financial services and products. Bud has many products that serve both consumers and businesses. For instance, Bud users can manage all their bank accounts in one view while also tracking their carbon footprint and making a purpose-driven, sustainable impact with their money.

What’s more, Bud’s data intelligence capabilities help users identify their spending on subscription products like Netflix and allow them to manage their subscriptions from inside their primary bank apps.

This list covers just a few exciting examples of payment solutions companies that have harnessed the potential of open banking. New players are constantly arriving in the market, enhancing payment services and our daily financial routines.

There’s no doubt that open banking is here to stay. The main question is, what does its future look like?

Will open banking payments go mainstream?

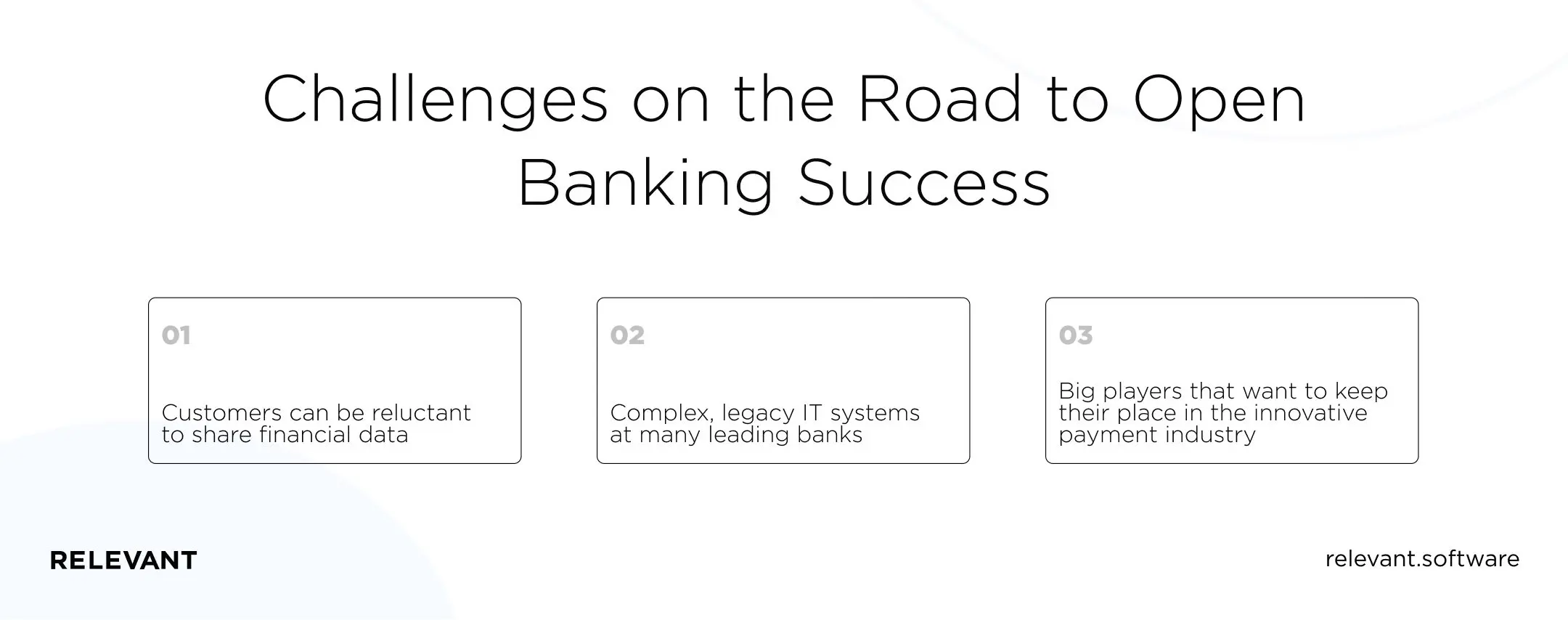

Open banking is only just kicking into gear. The concept has created a significant market opportunity and has the potential to change the competitive landscape of financial services. Yet, despite the many benefits open banking offers, there are also significant challenges to its wider adoption.

One major hurdle is consumer perception. For example, Deloitte’s consumer research reveals a strong demand for new and improved banking services among a technologically savvy population. However, customers can also be reluctant to share financial data unless they’re sure that it is handled securely. This makes consumer education and security compliance a priority for anyone wanting to enter the market.

Another barrier to open banking adoption lies in complex, legacy IT systems at many leading banks. For open banking to succeed, banks must embrace a new end-to-end digital architecture. This requires a significant investment of time, effort, and financial resources, which naturally slows down the process.

Finally, big players like Mastercard and Visa are also considered a threat to the open banking ecosystem. It’s unlikely that they’ll buy up all the open banking startups, but they’ll probably want to keep their place among the industry’s innovative payment solutions.

Despite all these challenges, the future of open banking is definitely “open.” The movement just needs time to fully evolve on a global scale—just like any other fundamental change.

Summing it up

Open banking is no longer a technology of the future. It’s already with us. And it will continue to evolve as it connects more and more banks and fintech businesses, increases competition, and accelerates the development of new products and services.

Choosing the right software development company to build your open banking solution isn’t easy. Before hiring app developers, you should pay attention to their expertise and the technologies they use, as well as successful cases in their portfolio.

At Relevant, we’re ready to help you with banking software development and open banking adoption. Our experts can:

- Advise you on the open banking implementation and regulatory compliance

- Create the UI/UX design for your online payment solution

- Pick the most relevant tool stack for your needs

- Help you build your own software payment solution or embed a payment gateway into your application

Whether you’re planning to develop your own fintech app or platform, add open banking to your services, or just want to receive a consultation, contact us. We’ll be happy to help.