ISO 20022 Overview: Migration and Adoption

Andrew BurakCEO and Founder at Relevant Software

Andrew BurakCEO and Founder at Relevant Software

More countries around the world are embracing the financial Standard called ISO 20022. As predicted, by 2025, ISO 20022 will be the de facto standard for high-value payments systems of all reserve currencies. But what’s the story behind it?

In our article, we’ll give you the most useful information about what ISO 20022 is, how it is different from the other standards, its benefits and challenges, and much more.

Let’s start with an example. Someone in the U.S. transfers USD100 to a friend overseas. However, the way the sender’s bank phrases the message on the transaction is not synonymous with your bank’s formats. With some details missing or vague, that transaction may be difficult to process. When your organization processes a Single Customer Credit Transfer, you need the institution initializing the transaction to provide a detailed message. Failure to do so would mean the transaction will not go through.

Standardization bridges the gap. And ISO 20022 is the new standard that’s incorporating more definitions to cut across regional and geographical divides.

The challenge and impact of ISO 20022 for banks

Although banking and finance happen to be the most regulated sectors across the globe, different geographical areas have their own communication standards. Over the years, organizations like the Society for Worldwide Interbank Financial Telecommunication (SWIFT) and the International Organization for Standardization have worked to standardize how messages are sent back and forth to confirm and authenticate a transaction.

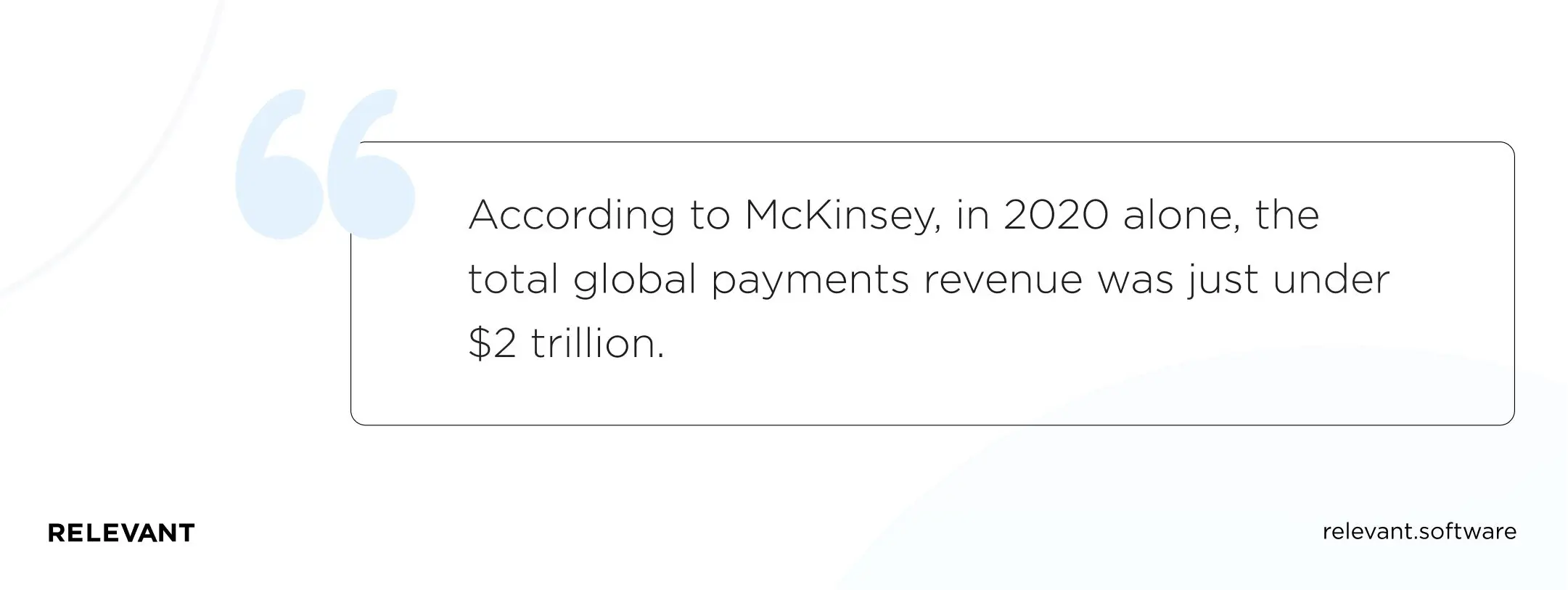

In today’s business environment, speed is everything, and lack of standardization reduces the speed at which transactions are processed. Not to mention the risk involved with miscommunication between banks when big sums of money are involved. According to McKinsey, in 2020 alone, the total global payments revenue was just under $2 trillion. If institutions from different regions are using different standards when it comes to communicating these transactions, streamlining and syncing global banking becomes a tough job.

Currently, most cross-border transactions operate on fragmented standards that are subject to local practices and their variants. As a result, it is difficult to manage communication between Financial Market Infrastructures (FMIs), Financial Institutions (F.I.s), and machines. It would be easier if these separate entities communicated using a single language. Standardizing payment technology this way will improve efficiency in payment processing and boost data automation capabilities internationally. With globalization, the need for interoperability has significantly increased. And this is why the adoption of and migration to ISO 20022 payments is necessary.

[e-book id=”6910″]

A brighter future with ISO 20022

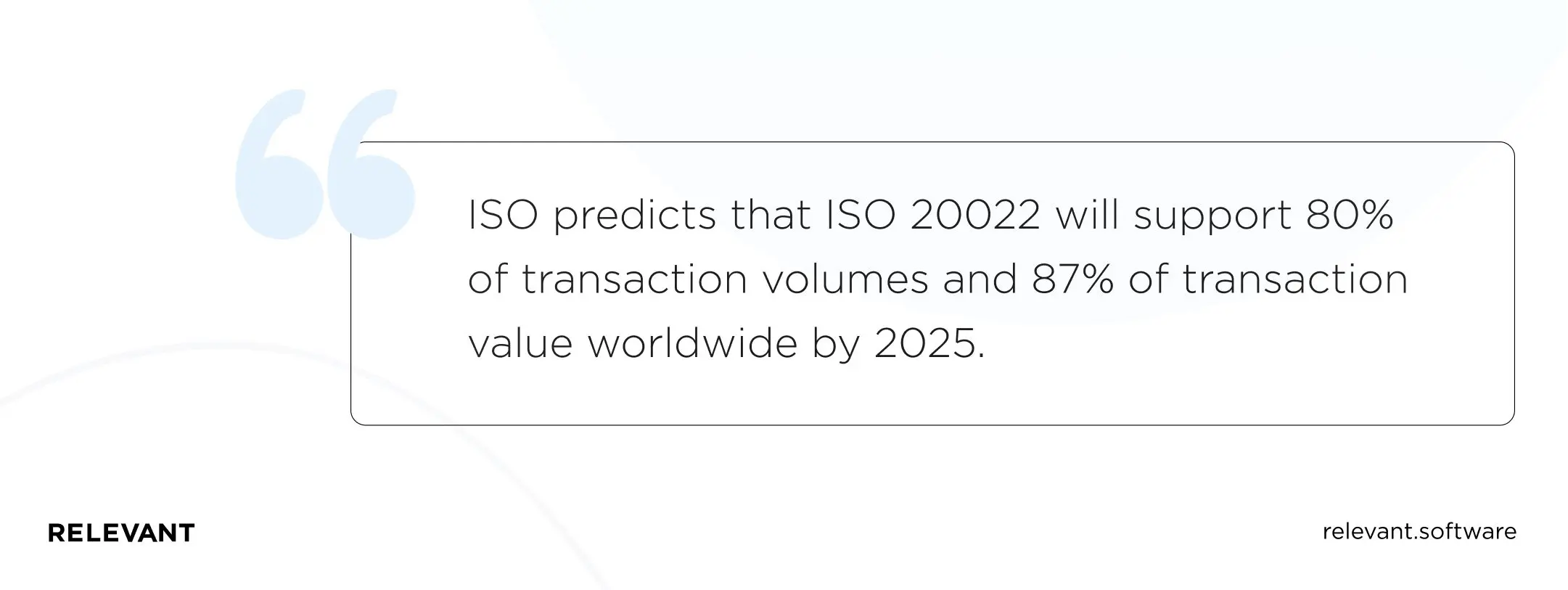

ISO predicts that ISO 20022 will support 80 percent of transaction volumes and 87 percent of transaction value worldwide by 2025. In Europe, the deadline previously set was extended from November 2021 to November 2022. SWIFT and the European Central Bank have both announced go-live dates for 2022.

With all these changes taking place, businesses also have to think of the technical aspects. Naturally, SWIFT will be proposing out-of-the-box solutions. However, these may have limitations and fail to meet an organization’s needs. Hence, custom solutions. More agility will be necessary to accommodate the SWIFT changes; financial institutions will need to build flexible functionality into their fintech and banking apps.

Read on to understand how ISO 20022 works. Discover how to get a system native-built for ISO 20022, without a hassle. As the new standard comes into effect, there’s a need to dig deep into its impact on the future of banking.

ISO 20022 basics

ISO 20022 is a worldwide financial messaging standard meant for financial institutions. This standard was developed by the independent standard-setting body known as ISO, acronym for the International Organization for Standardization. The ISO 20022 language is based on a business dictionary that combines several existing, separate standards. It incorporates huge amounts of highly organized data in a manner that will add great value to market participants.

The effects of ISO 20022 extend to financial institutions, corporations, developers of payment systems, trade bodies, and industry groups. The available data sets will boost end-to-end automation via the transaction life cycle and promote machine readability. This will enable speedier processing, increased openness, visibility, and interoperability across different regions.

ISO 20022 and other standards

Before the introduction of ISO 20022, there were several other options available for standardization. Here is a brief review of how this new standard differs from its predecessors and alternatives:

ISO 20022 vs 15022

ISO 15022 was developed in 1995 to offer the securities industry a more effective tool for greeting message standards. The former standard ISO 7775 featured actual messages like those found on SWIFT MT. ISO 15022 doesn’t contain the actual messages; instead, it features a set of rules and guidelines that are used to come up with messages. If one adheres to these rules and guidelines, the message produced is therefore in ISO 15022 format.

ISO 20022 is the successor to ISO 15022. The main difference between the two is that with ISO 20022, messages are more versatile and less tied to specific formats. This boosts the quality and accuracy of data sent between payments, securities, and internal systems.

ISO 20022 vs. Swift MT

About a decade ago, SWIFT came up with a set of formal specifications that outline how to change a limiter amount of M.T. messages into their ISO 20022 equivalents. This was in an attempt to ensure that SWIFT MT and ISO 20022 can coexist. ISO 20022 formats are usually more comprehensive than SWIFT MT formats.

Currently, it is possible to map M.T. formats to and from ISO 20022 formats. SWIFT also offers an ISO 20022 translator that can be used as a standalone or as part of the SWIFT interface.

What makes ISO 20022 so great?

Multiple financial systems are slowly moving towards adopting ISO 20022 because of the numerous benefits it offers format-wise. The standard is reputable for:

- Simplified processes

- Lower costs

- Lower risk of data manipulation at interbank

- Reduced manipulation of data banks & customers

ISO 20022 enables international corporations to use the exact data format in all the countries they do business in. It also makes it possible for suppliers to get data from businesses without worrying about losing or misunderstanding the data. That is part of why ISO20022 is so great. There is no need for translation; therefore, information flows smoothly.

The other reason corporates find ISO 20022 so attractive is because it’s bank agnostic. Companies that use it find it easier to communicate with their banks in a more consistent fashion.

And then there is the factor about regulation. For a long time, regulators found it rather challenging to use disparate messaging formats. The complaint was that they resulted in payments being sent with missing information. This caused severe hardship for the compliance officers. But now, with businesses adopting ISO 20022, the authorities will find it easier to do their jobs. On the other hand, corporates will start viewing regulation and compliance as a business expense rather than overbearing restrictions that need to be worked around.

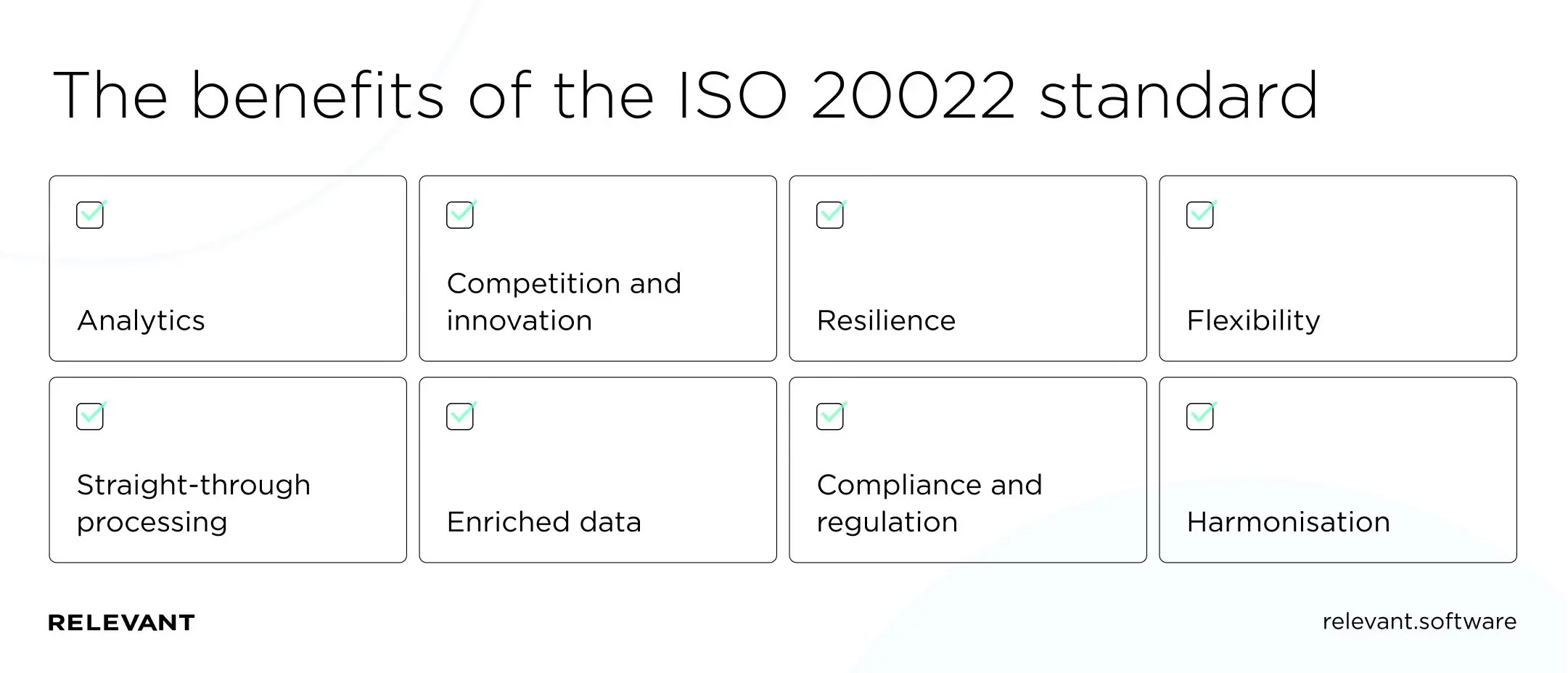

To sum it up, here is a list of the benefits:

- More structured data is available; hence enriched financial data

- Efficient data collection and robust analytics

- Enables automation as less manual interventions will be necessary

- More flexibility

- More room for innovation at a global scale

- More resilience driven by the ability to reroute messages

- Improved compliance and regulation

The challenges and impact of ISO 20022 for banks

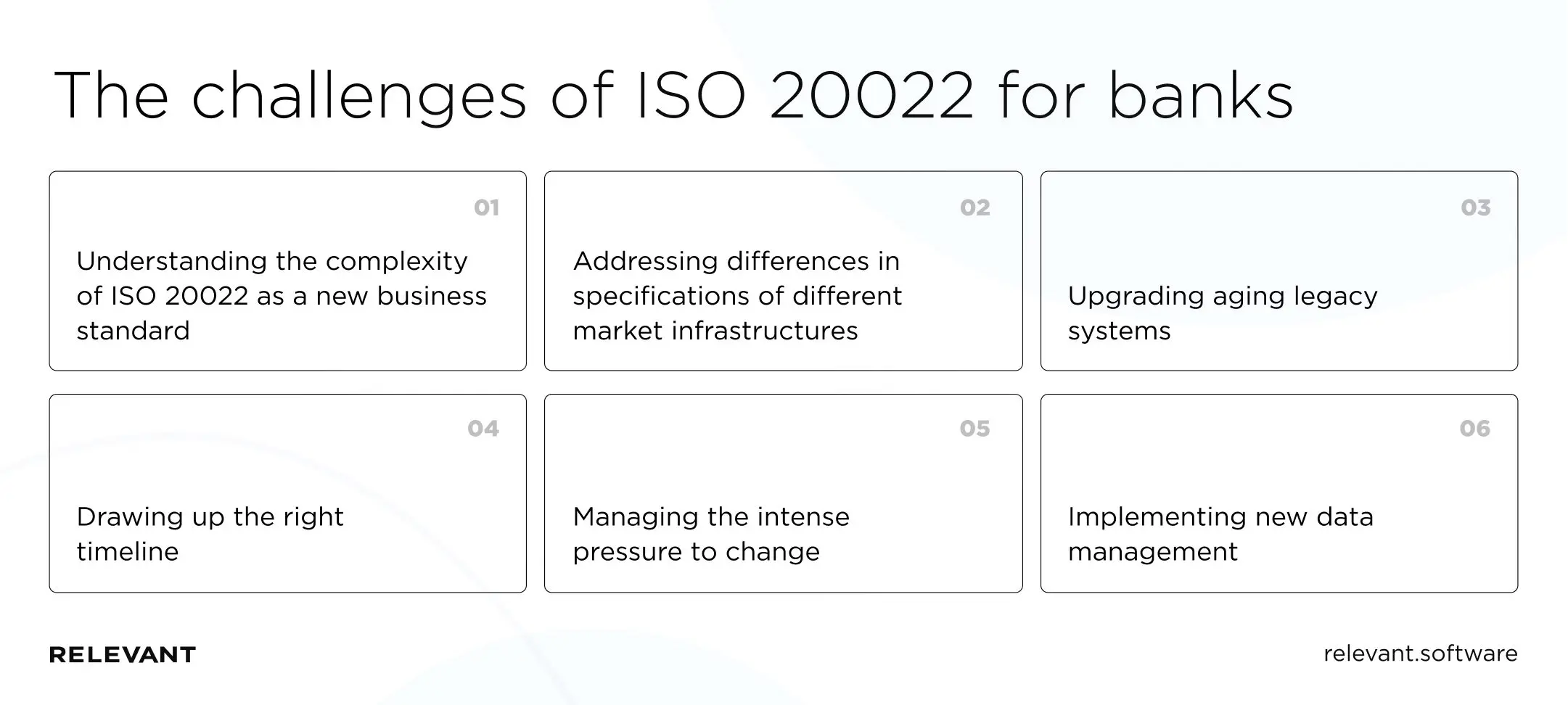

Banks are currently facing tight compliance deadlines for ISO 20022. With ISO 20022 being as complicated as it is, meeting these deadlines is going to be difficult. Banks need to understand how ISO 20022 works and quickly adopt it as the new business standard. This creates a need for a translation system that will be used to map older systems to this new standard.

Banks and other companies that offer financial services also face the challenge of addressing the differences in specifications for different market infrastructures. Furthermore, the process of upgrading old legacy systems is not going to be easy and cheap. These systems cannot work alongside ISO 20022; therefore, they need to be replaced. In cases where it’s not possible to replace them, banks can protect themselves by using translators and similar software.

There is a need for detailed timelines regarding when banks will start ISO 20022 implementation and include its guidelines into their systems. Different countries and regions may take it up at different paces, but ultimately, the goal is to have broad adoption by the end of 2022. This migration has to be carefully planned so that the entire banking industry remains in synchrony.

Banks are already feeling the pressure to change. There are a lot of other things that banks will be handling, and the current migration only adds to that pressure. Because of the structure of ISO 20022 messages, banks also need to redefine all the infrastructure that will handle data. All these challenges require banks to have a tight and well-thought-out migration strategy.

ISO 20022 for fintech

As banks and other financial institutions continue to migrate to ISO 20022, a lot of the dialogue in fintech is eventually going to focus on this new standardization of language and messaging for payments data.

Businesses have been preparing for and adapting to ISO 20022 for the past 15 years. Because of the difficulties the entire world has been facing in the past year or two, the significance of ISO 20022’s aims has never been clearer. It has become more important now than ever for companies to manage their cash better as they are fighting for survival.

The global Fintech industry is unified in its efforts to address the challenges of local and international payments. ISO 20022 seems to provide a lot of the answers needed on that front. It will therefore have resonance across all major developments in the Fintech space.

Choose Relevant fintech development services

Organizations that want to get ahead will need a reliable technology partner, so they can focus on streamlining their internal processes rather than the tech. More entities are relying on APIs and ISO 20022 to usher in a new standard for global payments. Currently, European and Asian banks are already far ahead in terms of adoption.

At Relevant Software, we provide businesses with superior tech talent and product development expertise to craft world-class software. We have been providing fintech software development services for seven years now and operate worldwide. One of our goals is to offer businesses an affordable way to build effective Fintech Software by working with our dedicated software development teams. Our skilled team is able to build fintech apps, online banking software, bookkeeping software, and trading and exchange platforms.

One of our recent noteworthy products is FirstHomeCoach, a fintech platform quite handy for those that want to buy property in the U.K. It simplifies purchasing property, access to trusted advisors for securing mortgages, insurance, and legal paperwork. With our help, the UK-based fintech was able to launch a product that matches their vision and meets the user’s expectations.

With a robust technology stack encompassing React, Node.js, Java, Python, cloud infrastructure, and more, Relevant is equipped to help financial institutions minimize disruption as they embrace ISO 20022. Our team can empower banks, trade bodies, and fintech operators to translate between traditional message formats and data-rich ISO 20022-based messages. And beyond that, we build solutions that deliver intelligent processing across channels, payment types, different market infrastructures, and communication capabilities.

Summary

ISO 20022 migration will probably serve as a test for how various businesses and institutions in the finance space can adapt. The major drawback that larger incumbent banks might face is the size of their legacy systems. It might be quite challenging for them to migrate and adopt IS0 20022.

This raises the question of whether newcomers and smaller institutions will have a competitive advantage over large banks and financial institutions. It will be easier for them to join the adopters of ISO 20022 and quickly migrate to ISO 20022. Additionally, some of them might even be built with the ISO 20022 standard in mind. Migration to ISO 20022, therefore, presents several advantages and challenges. Feel free to browse our fintech app security solutions and look at some of our case studies to find out how our solutions can help your business.