Need to Build a Credit Scoring Software Solution? Read This First

A single three-digit score no longer decides who gets a loan. Lenders now read hundreds of data signals and let AI weigh them in seconds. The money is following: the AI in lending market is on track to reach about $14.71 billion in 2026.

Instead of relying on the limited and standard traditional credit score, many banks and financial institutions are now using credit scoring software to measure qualitative and quantitative risk factors before financing individuals and SMEs.

To quicken the process and expand loan disbursement, technological advancements in Fintech are reshaping the lending landscape, bringing in new ways to help borrowers easily access loans.

Popularly known as alternative credit scoring, these methods enable lenders to qualify for a loan even without a good traditional credit score.

Over the past few years, credit scoring software has garnered mainstream appeal from both financial institutions and borrowers. Alternative credit scoring uses digital software to assess the applicant’s creditworthiness.

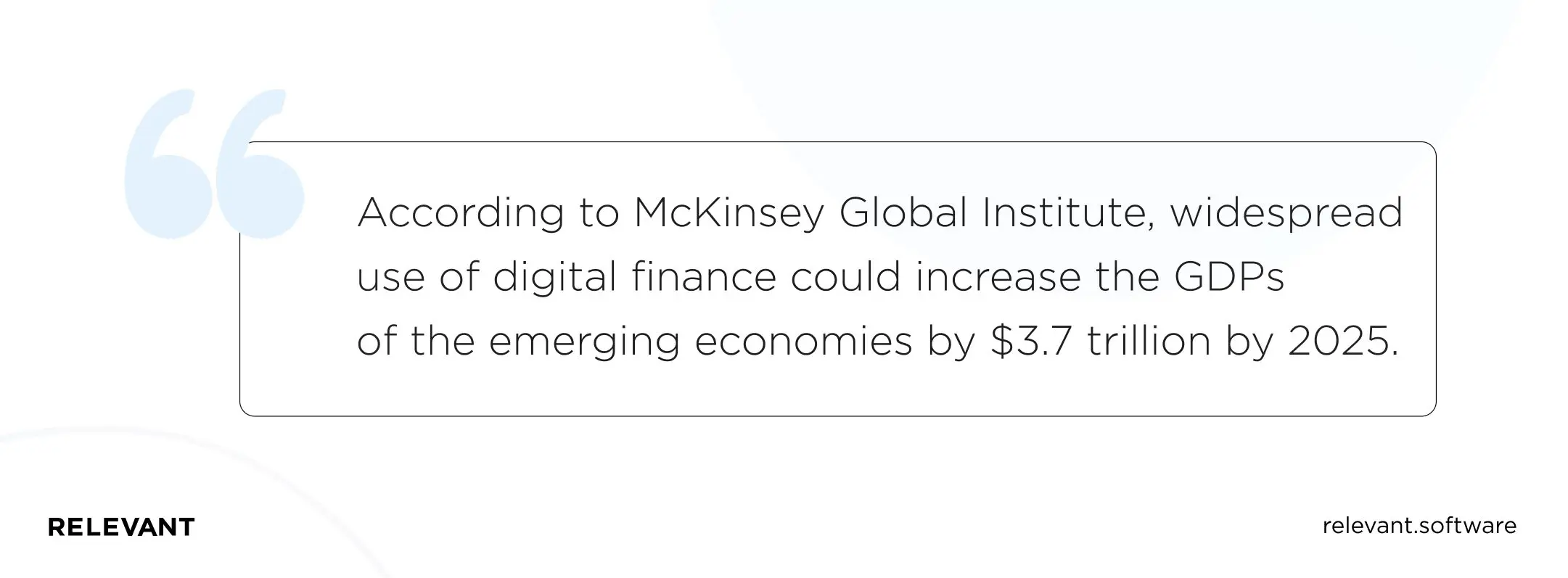

McKinsey Global Institute (MGI) found that the widespread use of alternative digital financing could boost the annual GDP in developing economies to about $3.7 trillion by 2025.

The unprecedented growth in the use of mobile phones globally is one of the primary driving forces in the evolution of alternative financing.

How is technology changing the lending market?

New technologies are disrupting every industry, and the lending industry is no exception. Mainly, four factors are driving the digitalization of consumer financial services. These include:

- The necessity to simplify the existing processes

- Dynamic consumer behavior

- Changes in regulations and compliance

- Rapid technological advancements

The combination of these factors has influenced an era where consumer insights are blended with product innovations. This makes fintech consumer lending more inclusive.

Rather than focusing on high credit-worthy consumers, the future of the lending market is influenced by the need to involve potential customers with a low credit history. These include freelancers, students, low-income households, and many others.

Traditional approaches such as the FICO credit scoring are quite limited when it comes to showing an applicant’s creditworthiness.

Technology is ushering in new ways to vet loan applicants. One of the key technologies financial institutions are adopting is artificial intelligence.

AI helps in the development and adoption of new credit score models. The new models include various data points, such as spending habits, education details, and employment history, among many others.

This information can verify if an applicant’s potential to clear their debts in time.

Digital lenders are now partnering with app development companies to create AI-powered credit scoring solutions.

The powerful algorithms can help confirm and validate whether applicants are telling the truth regarding their income level.

Additionally, lenders are using blockchain to develop low-cost and high-trust platforms while eliminating the need for intermediaries and third parties.

What is traditional credit scoring, and why is it not effective?

Traditional credit scoring is a lending method where financial institutions consider the applicant’s number of open accounts, payment history, credit utilization ratio, and current debts.

Using this data, the Consumer Financial Protection Bureau found that 54% of USA adults had a favorable credit score. Moreover, there is a much lower number of people in developing countries with access to reliable data. Thus, traditional crediting is only effective in developed countries.

Did you know that more than 1.4 billion people do not have access to traditional financial services?

While traditional credit scoring methods are highly predictive, the information used to produce them is limited because they are dependent on data from centralized credit bureaus.

Emerging or developing markets find it hard to use bureau data because it is usually entirely unavailable or incomplete.

The World Bank found that less than 10% of people in developing countries have credible information in public credit registries.

Switching from traditional credit scoring methods to alternative finance could therefore help reduce corruption in emerging markets and save their governments $110 billion.

What are the advantages of alternative credit scoring?

Alternative credit scoring is beneficial both for borrowers and lenders.

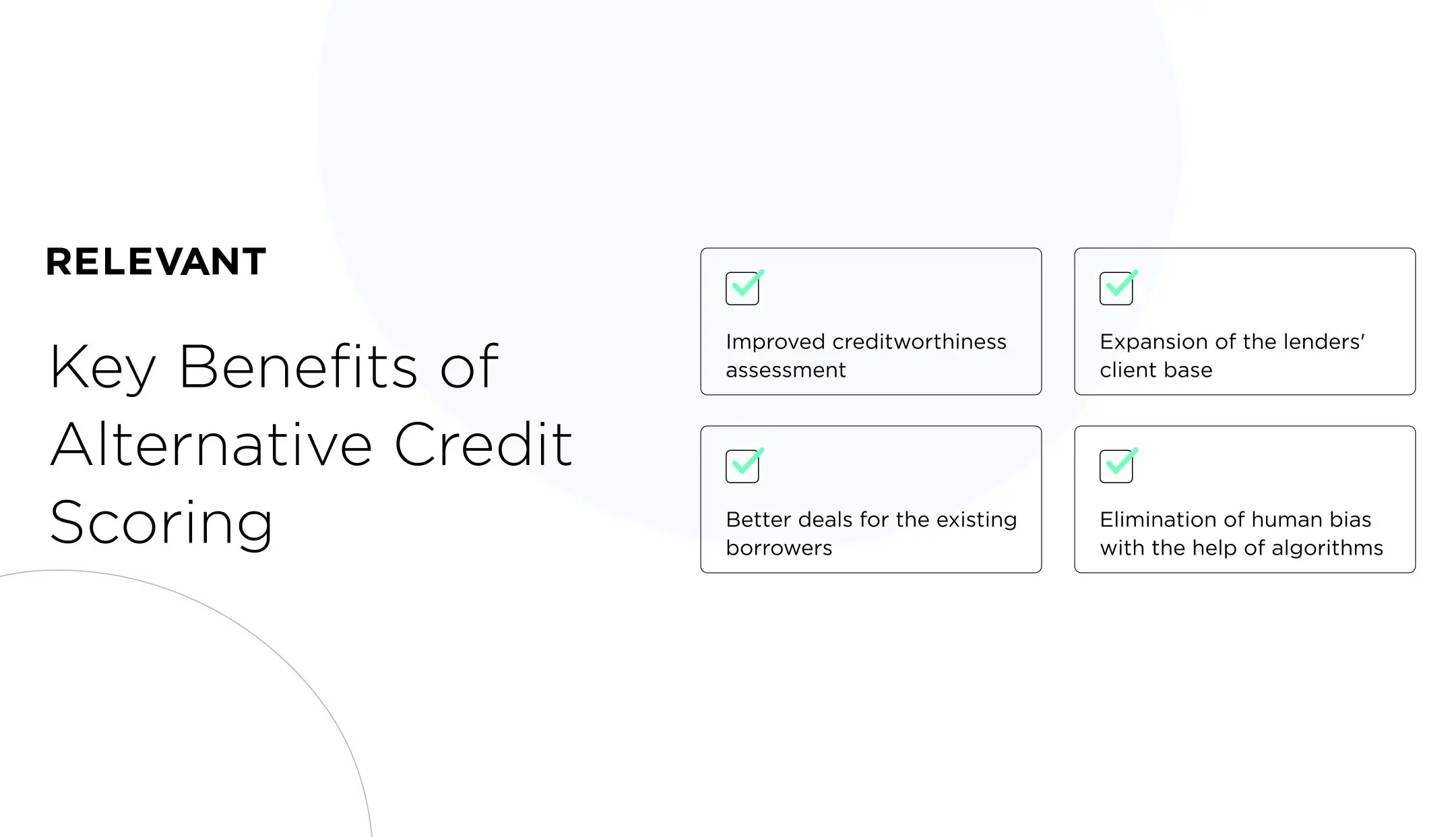

Alternative credit scoring is the perfect solution for young people, individuals with no credit history, and adults with stale or thin traditional credit scores. Alternative credit scores help them not only qualify for loans but possibly under better terms.

The main benefit of alternative credit scoring in fintech companies is that more people qualify for loans.

Furthermore, financial institutions can distribute loans with a more accurate understanding of the scoring credit risk involved. This can expand the lenders’ client base and also protect them.

The additional information gives borrowers an edge and more control. They can customize their alternative credit scoring, something impossible with traditional credit scoring.

The current state of alternative data

Big data is on the rise, and like every other industry, the lending landscape is also making major strides to use consumer data. This has a huge impact on alternative credit data.

The new sources of information benefit both consumers and lenders, particularly the latter, since they can consider many factors to make insightful and regret-free credit decisions.

Financial institutions are identifying new ways of utilizing consumer-permissioned data. Accessing data directly from consumers’ financial accounts gives lenders a fuller financial picture and boosts risk assessment.

Since consumers are now providing digital permission to lenders, it has led to faster decision-making. Therefore, utilizing new data sources, such as rental payments, account aggregation, and on-time utility, lenders can have a more holistic view of consumers.

How fintech companies implement alternative credit scoring

Economic shocks, from job losses to inflation, regularly push people into thin-file or damaged-credit territory. That hurts both their finances and their credit score.

Today, millions of people globally have little or no savings to cover emergencies, while their inability to pay existing debts further negatively affects their credit scores.

Fortunately, fintech companies are no longer relying on traditional credit scores.

Using alternative credit data, lenders can now boost loan approval rates and consequently reach millions of people whom traditional scoring would simply turn away.

Alternative credit scoring provides supplemental information about consumers who do not have sufficient traditional data.

Some lenders, such as CreditLadders, allow applicants to use their rent payment history. While other lenders analyze the applicant’s lifestyle, professional background, spending habits, and financial situation.

Today’s fintech companies rely on credit scoring software to build alternative credit profiles. This allows lenders to build a complete profile of their applicants and use it in their decision-making process.

For instance, a Singapore-based lender called Lenddo uses multiple data points such as smartphone data, geolocation, browsing behaviors, and social media activity to analyze applicants’ creditworthiness.

Additionally, some credit scoring innovators use other algorithms in their credit scoring app development to assess creditworthiness. For example, a US-based start-up called Tala uses credit scoring algorithms based on applicants’ online activity and phone usage patterns to determine whether they can offer a loan.

Another micro-lender is dependent on data from applicants such as text and call logs, GPS information, contact lists, and their interaction with the Branch customer services and platform.

On the other hand, another digital credit scoring platform, Deserve, provides credit cards to applicants in the US without a social security number or a credit history. Instead, they rely on the applicant’s bank account activity, such as regular on-time payment of bills and stable income.

Providing credit directly, building alternative credit profiles, or supplementing traditional credit scoring models are just but a few of the innovative solutions by various lenders.

Thanks to credit score software development companies, credit is now more affordable and accessible to previously underserved segments.

Furthermore, alternative credit scoring machines are enhancing risk analysis for lenders, sharpening the accuracy of their existing data algorithms.

Lenders are relying more on machine learning technologies to boost their processes through reliable data. And predictive models used in alternative data are becoming increasingly reliable in analyzing applicants’ creditworthiness.

As such, credit scoring in fintech companies is now more important than ever.

Machine learning and credit scoring: How does it fit-in

Machine learning plays an increasingly important role in business and technology. Particularly, machine learning is a helpful tool for building powerful credit scoring platforms.

Machine learning helps computers not only analyze data, but learn from it and make reliable predictions using the new data. Instead of simply hand-coding a unique set of instructions to accomplish certain tasks, the machine is “trained” through a large number of algorithms and data to make decisions.

This allows the machine to improvise and perform new tasks. At present, the major companies using machine learning include Netflix (for movie recommendations), Facebook feeds, and Apple’s Siri.

When you or a business apply for a loan, the lender evaluates whether the applicant can repay the loan principal, including interest. Lenders often utilize measures of profitability and leverage to assess risks.

Machine learning methods allow lenders to learn from data without using rules-based programming. Therefore, machine learning is flexible and can better fit various data patterns.

While many people across the world have never obtained a bank loan, they are usually active mobile phone users who have a healthy social media presence.

Machine learning can use traces of these unstructured data based on their mobile phone usage and online behavior to make factual conclusions. This allows the company to predict and analyze its behavior by default.

Consistent with this idea, numerous fintech companies have grown all over the world with the objective of closing the lending gap.

Fintech companies are now leveraging machine learning, big data analytics, and unstructured data to process loans and help as many people as possible.

Credit scoring software solution: How to build one?

Creating a credit scoring software is quite complicated, but it’s no rocket science. Before diving into the complex technicalities, you need to have a clearly defined and consistent scoring policy.

What should you consider when building a credit score solution?

There are many factors to consider when developing credit scoring software. For starters, you need the right data, you might use the most innovative algorithm but without important data, it’s all in vain.

- Define the major business objectives around scoring credit

- Double-check if you have enough data

- Consider implementing AI and ML to improve efficiency

Credit scoring solution implementation

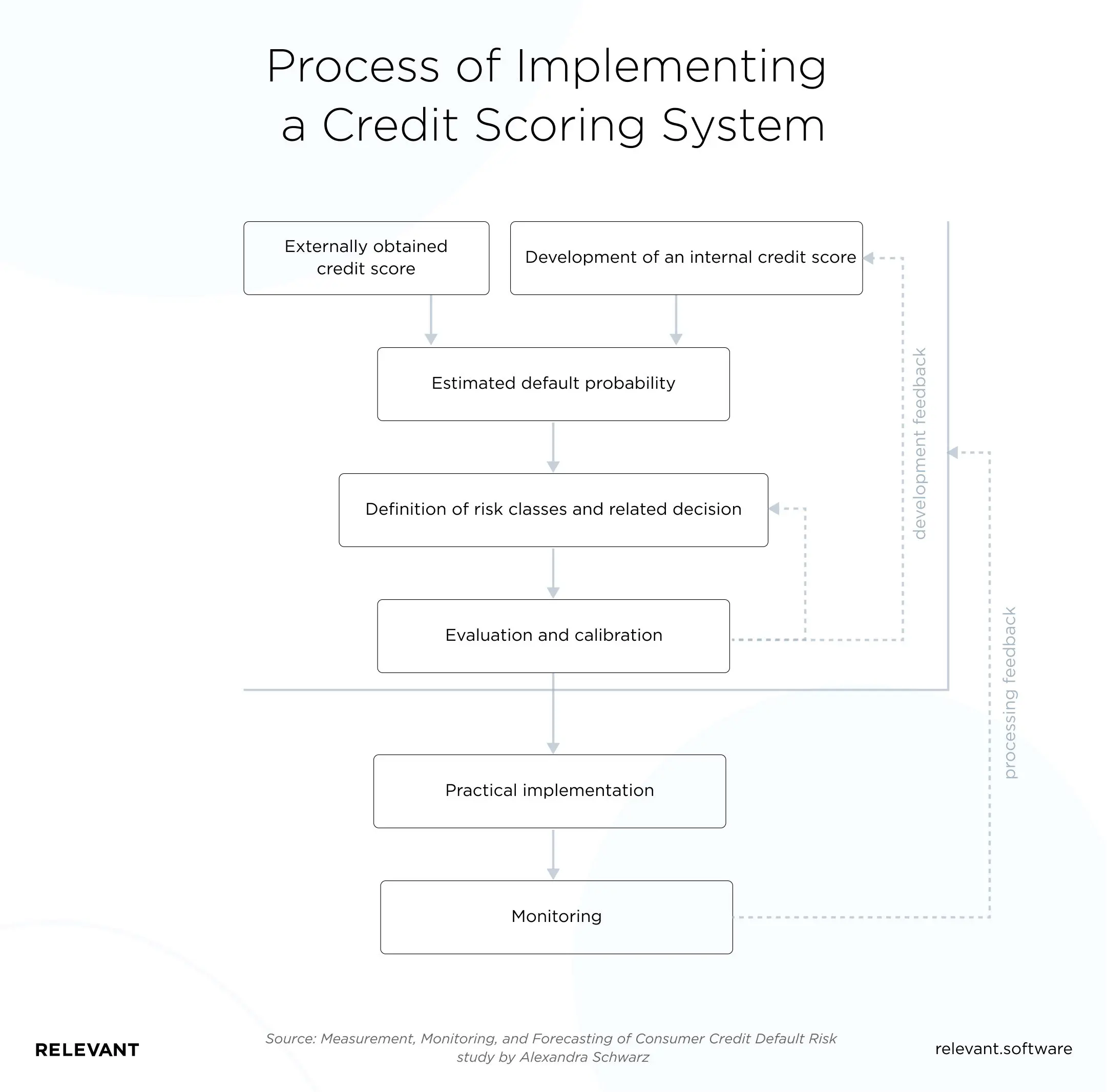

The implementation of a credit scoring system includes the following steps:

- Acquiring credit score: This can be done internally or externally. The preliminary process includes acquiring all the relevant data to come up with a statistical credit scoring analytics model. ‘

- Estimated default probability: The lender should identify borrower characteristics linked with users who are unlikely to repay loans.

- Determining risk classes and related decisions involves determining cut-off values on their probability scales, assigning applicants to risk classes, and making class-dependent decision rules.

- Evaluation and calibration: Involves back-testing of the available custom credit scoring engines and systems, such as managerial advice, classification, and credit score.

- Practical implementation of the credit score solution according to reliable risk management policies.

- Monitoring: It involves observing and monitoring credit/debtor data and their payment behavior.

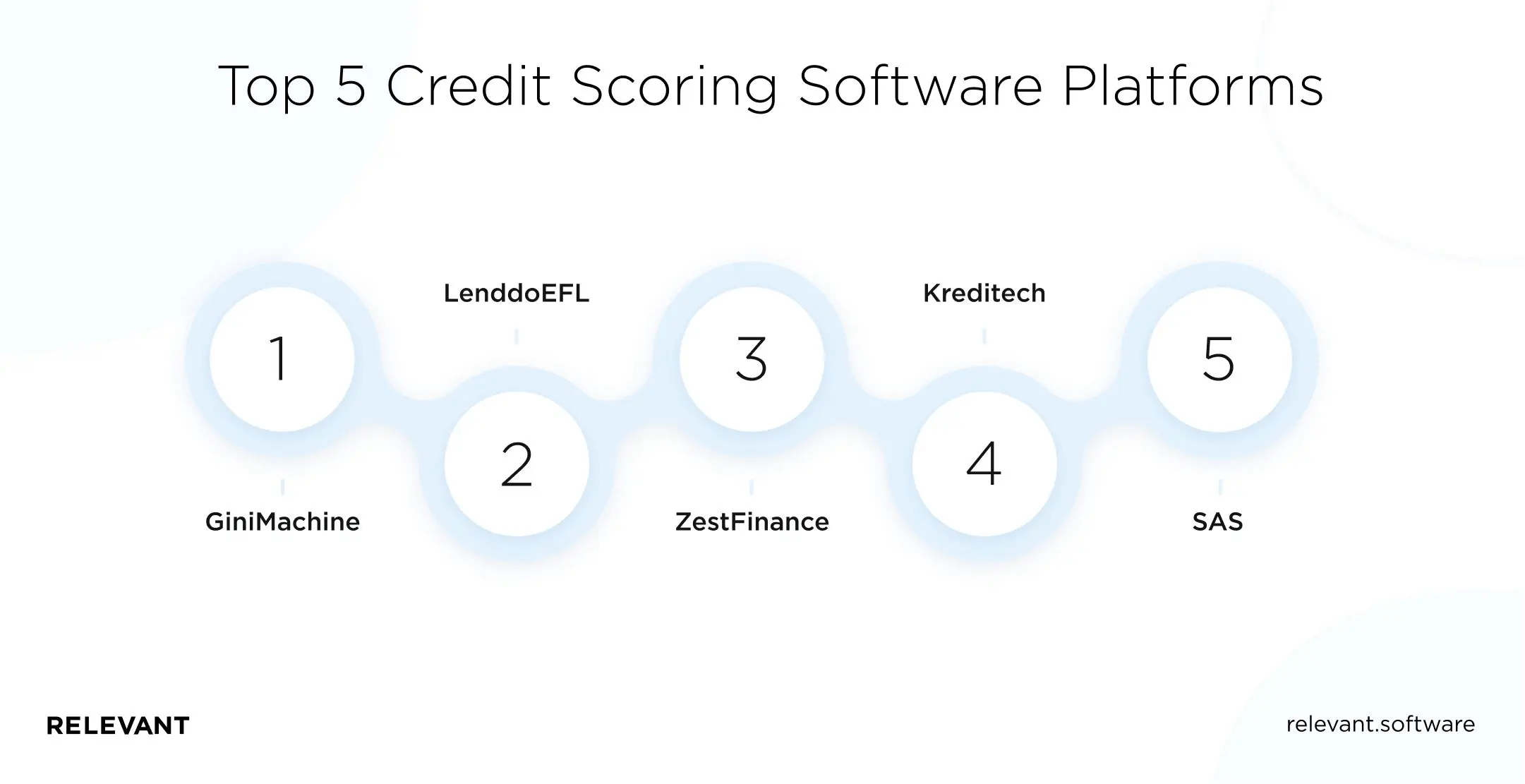

Top 5 credit scoring software platforms

Here are some of the best credit scoring solutions you should know to better understand how these systems work.

1. GiniMachine

GiniMachine is an innovative credit scoring solution that uses your historical data and advanced machine learning algorithms. This platform automatically creates, validates, and implements high-performing risk models.

Additionally, it utilizes artificial intelligence and machine learning to build credit scores for both business and consumer lending.

Unlike the average credit scoring solutions out there, GiniMachine reduces non-performing loans by about 50% and allows applicants to get a two times higher acceptance rate. More so, the platform can boost loan portfolio returns by about 30%.

There’s more! GiniMachine builds, validates, and deploys models within an hour, allowing you to develop scoring models in a matter of minutes.

2. LenddoEFL

LenddoEFL is one of the authority companies in credit scoring development.

Their app allows SMEs and individuals to access financial services privileges using their digital footprints. Lenndo’s patented score is one of the most potent indicators of an individual’s willingness to pay or character.

The credit score ranges from 1 to 1000, and higher scores represent a lower probability of default. The Lenddo score is often used at the wide end of the funnel, when prioritizing applications.

Moreover, it can be used with existing underwriting scorecards to approve more applications or reduce risk.

3. Zest AI (formerly ZestFinance)

Zest AI, formerly ZestFinance, offers a credit-decisioning app called ZAML. This app can potentially help financial agencies assess the creditworthiness of applicants and ease loan defaults using natural language processing and predictive analytics.

The credit score solution allows lenders to make quicker decisions, smarter predictions, and better lending. The software can increase approvals by 4%, grow yield by 4%, and decrease losses by up to 30%.

With clearer information about every applicant, smarter software, and more data, risk assessment becomes pretty easy.

4. Kreditech

Kreditech uses internal software to determine the creditworthiness of potential clients who do not have an extensive banking history.

Since they focus on applicants with non-existent or little credit history, Kreditech leverages artificial intelligence to help lenders make more accurate decisions regarding applicants.

Kreditech calculates a person’s credit score within seconds using about 20,000 data points. The company uses GPS, hardware data, social networking information, general online behavior, and online shopping behavior.

5. SAS

SAS has credit score software that claims to help banks and other financial agencies. They are focused on building, validating, and deploying more effective credit risk models through in-house expertise and predictive analytics.

The software can assess and control risks accurately using the existing client portfolios. They also analyze specific risk characteristics that lead to default, delinquency, or bad debt.

The company trained their algorithms to identify data points associated with borrowers who have a higher risk in comparison to others. Furthermore, it could help streamline applicant credit approval processes while improving acquisition, retention, and collection strategies.

This software could also help shorten data preparation time, understanding behaviors and relations. For instance, they can effectively develop scorecards and automatically create target variables.

Relevant case study: A custom mortgage solution for the UK fintech company

FirstHomeCoach is a UK-based fintech company that helps buyers simplify the complex process of purchasing property. The company connects them with trusted advisors to help them in handling all the necessary legal paperwork, for instance, when securing a mortgage or receiving insurance.

The client needed a custom algorithm and recommendation engine to evaluate loads of data and automatically plan their property buying process.

Fortunately for them, they came across Relevant’s dedicated software development teams. We helped them identify the technology stack, design the app’s architecture, as well as build the algorithm and system from scratch.

We delivered software that assists borrowers in developing a personalized plan while analyzing costs and recording every stage of the property buying process.

Additionally, the mortgage app integrates third-party facilities to improve user experience. The features include open banking solutions (e.g. open banking loans), credit reporting agencies, real estate companies, and banks to ensure a quick and easy process.

Our team paid utmost attention to how the app stores personal data to ensure tight security. Some of the implemented features include a property buying plan, mortgage calculator, deposit builder, and third-party integrations.

Relevant provides fintech software development services, and we specialize in financial app development. We helped FirstHomeCoach build a customized mortgage software that provides its users with a quick, smooth end-to-end home buying journey.

Wrapping up

Ukraine’s outsourcing is a great opportunity to develop a credit score system that suits you without breaking the bank. Whether your challenge is to enrich your software with new and beneficial features or build innovative credit scoring software solutions from scratch – we are here for you.

If you want to successfully implement a fintech project or know more about the solutions we offer, contact us!