Personalisation and Customisation in Digital Banking

Andrew BurakCEO and Founder at Relevant Software

Andrew BurakCEO and Founder at Relevant SoftwareHyper-personalisation is one of the largest trends in the banking industry in recent years. Due to AI and big data, personalised banking helps to deliver high-quality customer experience and attract new clients.

Relevant provides excellent custom software solutions, including those for fintech companies, which are known due to their hyper-personalisation technologies.

One of our finest projects is a SaaS platform FirstHomeCoach. It navigates buyers through the complex steps of purchasing a property. Due to its custom-made algorithm and recommendation engine, each client receives an individual property buying plan. They become owners of a dream house within a specific timeframe, based on their earnings, savings, and location.

Want to know how to adopt custom personalised fintech technologies from scratch or update your current banking products? How to use data customisation to make your service stand out? How to overcome hyper-personalisation obstacles and boost your revenue?

Let’s dig a bit deeper into the core points of mass personalisation in banking and see how this technological trend changes the present and the future of fintech.

What Does Personalisation in Banking Really Mean?

Personalisation in banking is not all about sales and growing revenue. Yes, you read it right. Hyper-personalisation is an approach that results in a unique user experience and high-quality service, every time a client works with a financial institution.

Clients of traditional banks often complain about the lack of understanding and cooperation from their financial providers. Why? Because most banks are simply trying to promote their services to as many people as possible. They do not dig deeper into the needs of each particular customer group.

On the contrary, such tech giants as Google and Amazon prove that resultative customised interactions with clients are real. Unsurprisingly, more and more people want the same high-quality service when they are managing their finances.

They want to do business with a bank that would help them solve their issues, rather than offering services they do not need. Mass personalisation in banking means that you get relevant recommendations and offers tailored to suit your needs and expectations.

How Banking Personalisation Boosts Revenue Growth

Customers are definitely looking for more personal engagement with their banks. With some fintech companies offering the first-class level of bespoke services, personalised customer interactions resemble communication with your personal virtual financial wellness coach.

But what about banks? Is hyper-personalisation profitable or loss-making?

Just like every being customer unique, the results of adopting hyper-personalisation would differ from bank to bank. There are no two personalisation plans that would be identical for different financial institutions.

First of all, revenue depends on how much money is invested in mass personalisation. Secondly, a more profound and well-thought approach will eventually lead to higher income. Scaling personalisation requires not only huge financial expenses but also revolutionary internal changes.

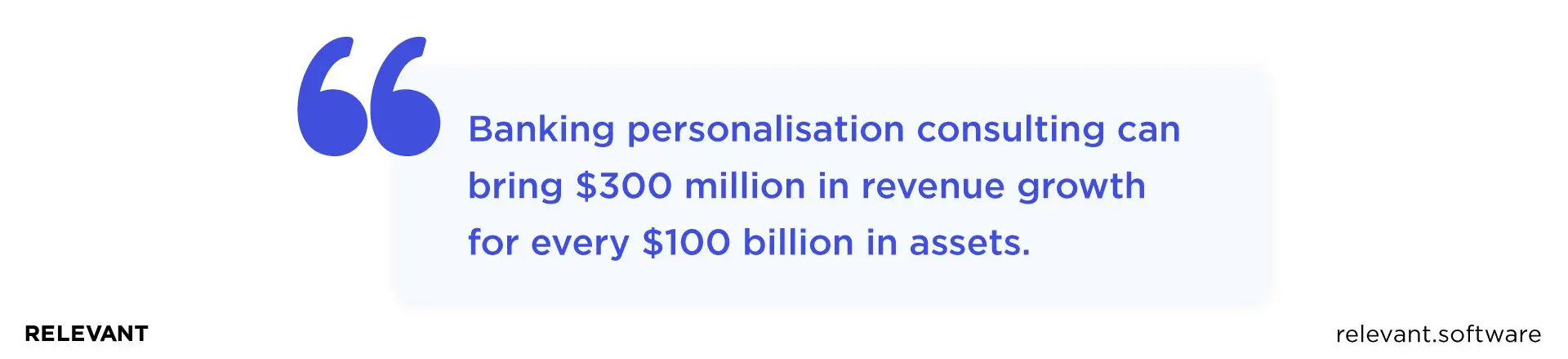

Thus, for some banks, a custom-built approach of communicating and providing services to clients can raise sales, while for some financial providers it can increase yearly revenues. According to the Boston Consulting Group, banking personalisation consulting can bring $300 million in revenue growth for every $100 billion in assets.

What obstacles are preventing banks from adopting personalisation?

Let’s get down to the obstacles awaiting banks that want to implement bespoke services.

First of all, banks are not using data analytics and behavioral science. Even though financial providers daily manage the data of thousands clients, they do not derive insights from the information received. To put it simply: banks need to move from a product-centric to a customer-centric approach.

The second obstacle for hyper-personalisation is that banks do not solve customers’ issues. Financial institutions rarely try to understand their clients. Indeed, most banks focus on selling their products rather than providing advice, guidance, and so-long-awaited solutions.

Finally, banks are not trusted. It’s pretty obvious once you think about it. We’ve all heard those stories about lost money, transfers that got stuck somewhere, and bank accounts frozen for months. What is more, such situations usually happen when you need money right away, which only adds frustration.

Consequently, when it comes to data sharing, customers are very suspicious. They do not understand who will have access to personal information, why it is needed, and how their data will be used.

How can banks overcome these obstacles to adopt personalisation?

By now, you’ll have realized that hyper-personalisation is, indeed, a little bit of rocket science. But no worries, let’s now check some tips on how to overcome the obstacles we discussed above.

Harnessing the building blocks of personalisation

What are the building blocks of personalisation?

These are behavioral science, data analytics, and ethnographic research. Harnessing such powerful tools enable banks to measure and predict consumer behavior and, what’s even more important, tailor their services and products accordingly.

Meeting customer needs

Any company has to be aware of customers’ needs to satisfy them. The same rule works for the retail banking industry. Investments in the abovementioned blocks of mass personalisation can help banks to study clients’ requirements.

But nearly every financial solution has exactly the same problem: they do not foster routine innovation. Hyper-personalisation is not something that can be implemented once and then work forever. On the contrary, customer-tailored service is about constant improvement, looking for better solutions, always seeking new ways to help clients. In such a way, banks can simplify and tailor their products and, what is more, make them available and affordable to a larger client pool.

Overcoming the data paradox

Let me show you how the data paradox works against financial providers. Many banks store department-specific information which usually has to do with their products or lines of business. However, they lack data on individual clients or customer segments. What do we have here? Lots of information but no practical use.

Relevant Software has been providing machine learning (ML) services for years now and we know how to leverage data for the best outcomes. In particular, ML is a key factor to overcome a data paradox. Due to smart algorithms and statistics, banks can gain valuable facts on their customers’ behavior and financial needs.

A Roadmap for Digital Banking Personalisation Initiatives

We’re done with all the obstacles and difficulties. Now, let’s have a look at all the tools that make mass personalization possible. In the picture below, you can see the roadmap for Digital Personalisation Initiatives. So let me show you how all the components of this roadmap work to sustain hyper-personalisation in banking.

Data lake

A data lake is a huge storage of all available information. It allows analyzing all information and receiving 360-view of all customers. A data lake is a foundation of hyper-personalisation because a bank cannot provide proper services without knowing who are its clients and what they want.

All this information is built upon systems of record and customer information. These include financial and transactional data, contract data, demographics, customer interests and behavior.

Advanced analytics

The role of advanced analytics is to gather actionable insights into customers’ behavior, preferences, and needs. It comprises customer segmentation, recommendation engine, and customer’s channel journey. Without these analytical tools, banks cannot tailor and improve their services to meet clients’ expectations.

One more curious and essential tool within advanced analytics is called the next best action. It requires a lot of good data and is simply the choice of possible suitable next actions for a particular client.

For instance, if you’ve recently converted some money into another currency, you might be offered to make a transfer or create a bank card for a new currency account by a chatbot. Such predictions based on customers’ behavior are, in fact, very useful because they save time and finances for both users and financial providers.

Digital banking experience

Digital banking experience combines content marketing, AI, multi-/omni-channel interactions, and on-demand customer support. All of these factors play a tremendous role when it comes to clients’ satisfaction.

In the modern world, communications are of the same importance as the services the company provides. With more and more people turning to banks to manage their finances, communications in the banking industry are also improving. For example, chatbots make interactions much faster and more efficient.

Also, many financial providers connect with clients via different messengers and social media channels so that customers do not have to wait for emails or phone calls.

Moreover, it is more convenient to use familiar messengers and receive instant feedback on their issues, rather than wait for hours on the phone till one of the support agents picks them up.

Personalisation in digital banking: 5 use cases

So how exactly does mass personalisation in digital banking look like?

Of course, there is no one recipe for tailoring financial and banking services to match the expectations of all clients. Nevertheless, the main idea behind bespoke customer services is a shift from offering all possible features to focusing and suggesting products that enhance client’s activities.

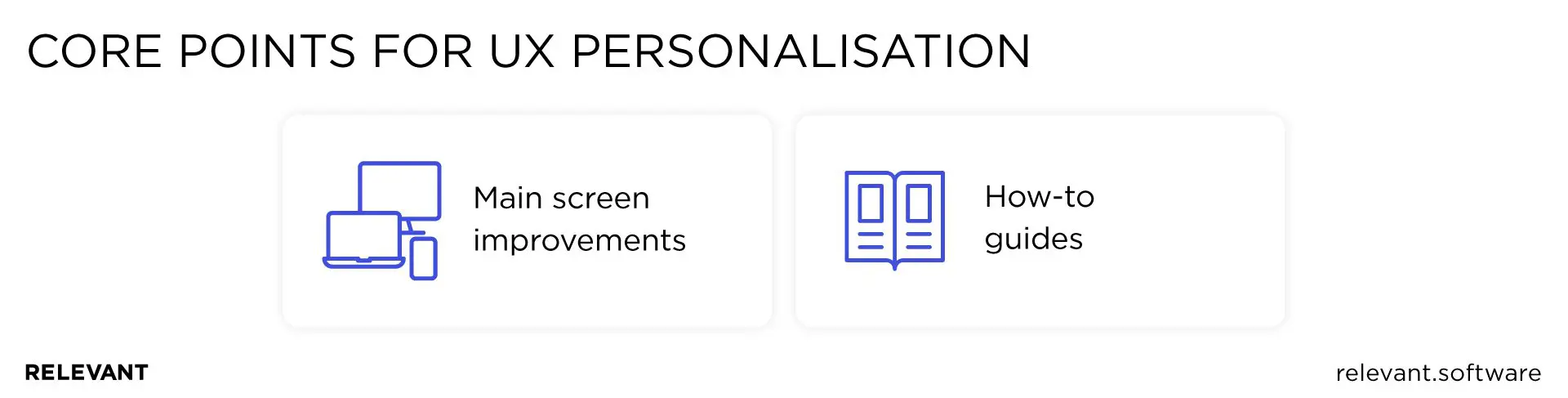

User experience and content are 2 core points for app personalisation.

UX personalisation

The quality of UX defines whether your clients will choose your service or switch to a provider with a better UX. UX personalisation in digital banking can be applied in the next fields:

- Main screen improvements

Changes in main screen functionality help customers to find the necessary buttons or information right away. A well-thought main screen design boosts clients’ satisfaction. For example, in JPMorgan Chase’s mobile banking app, Spanish-speaking people can choose the language even before logging in to the account. Thus, their UX becomes much more convenient and effective. - How-to guides

These features help to improve the quality and depth of use of a mobile application. In addition, such guides provide an overview of all available functions without having to talk to assistants. Finally, educated users can choose the services they need the most and use the features more efficiently.

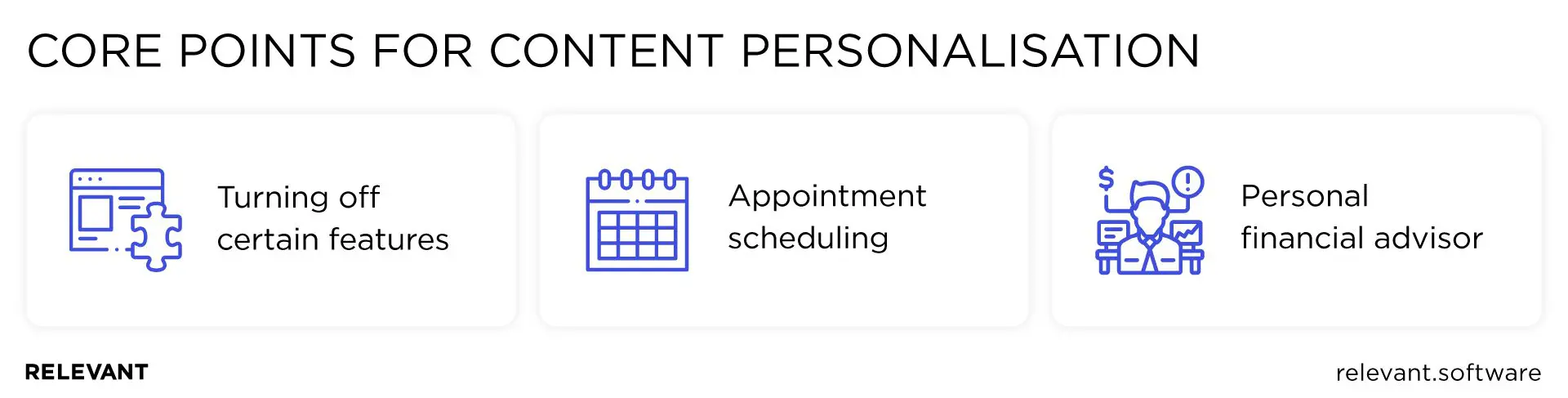

Content personalisation

Personalization of content depends, to a great extent, on customer segmentation. The division based on age, income, and other suitable criteria facilitates tailoring content as per the needs of a certain group of clients.

- Turning off certain features

Some customer segments, such as seniors, for example, do not need the whole range of banking features in their mobile applications. Consequently, the possibility to leave only the most essential ones will help them to make the most of a particular service. - Appointment scheduling

For some clients, banks may offer a special in-app scheduling function. - Personal financial advisor

With the help of data analysis, banks can recognize their users’ spending patterns and send notifications with warnings when the balance is critically low. The scope of such financial tips varies from bank to bank and depends on the analyzed information.

Entrust personalisation to Relevant

Mass personalisation in banking is a complex and challenging process, but personalised banking experience is what drives people to become loyal clients. Tailoring financial services to meet clients’ expectations is a huge digital transformation that requires time, efforts, and, of course, technological capacity.

In this article, we’ve covered the major pros of hyper-personalisation, the tools needed, as well as main obstacles and tips on overcoming them. Tailoring financial services to meet clients’ expectations is a huge digital transformation that requires time, efforts, and, of course, technological capacity. Thus, if implemented in the right way, high-quality bespoke banking services will benefit both the company and its customers in a long-term perspective.

If you’re looking for a reliable partner to adopt hyper-personalisation, Relevant Software is a great option. We provide fintech consulting and development services to clients all over the world. Do not hesitate to contact us for a consultation.