How to Build a Money Lending App: Relevant’s Guide

Borrowing has moved onto the phone. People now expect to apply for a loan, get a decision, and receive funds without setting foot in a bank. The digital lending platform market shows it, projected at about $16.45 billion in 2026 with double-digit annual growth.

One of the fastest-growing models is peer-to-peer (P2P) lending, where an app connects people who want to lend money with people who want to borrow it. No bank sits in the middle, so both sides can set terms that work for them.

This guide covers how loan and P2P lending apps work, the features they need, the stages of building one for iOS and Android, and what development costs to expect.

Building a money borrowing app: where to begin?

When you decide to build a money borrowing app, legal concerns and financial permissions must come first.

Start with selecting a legal entity form. The most popular ones are a Limited Liability Company (LLC) and corporation. Both will protect you from creditors in case of force majeure or bankruptcy, but they are taxed differently.

By default, an LLC is taxed as a pass-through entity, which means all profits and losses are reported on individual tax returns for its owners. On the other hand, a corporation is taxed as a legal entity that can generate income. Besides taxes on profits (corporate tax), there’s also a tax on dividends, which are, by the way, not tax-deductible (double taxation). With an LLC, the profits are accrued based on the agreement, while the corporation pays based on the number of shares of every individual shareholder.

Once you’re ready to proceed, you must register a business name within the country of your choice. Follow all the law requirements and pay the necessary fees, and, of course, think of a catchy name. If you decide to register your legal entity in the USA, make sure your trademark name differs from the legal name and is available at uspto.gov register of trademarks.

On top of that, you must secure the initial capital. This will be necessary for both peer-to-peer money lending app development and the first loans. Usually, investors are attracted to platforms like these only when they see users actually looking for loans there, so you need to have some funds to operate before the investor money kicks in.

There are three popular ways to secure the initial capital:

- Initial Coin Offering (ICO) or Initial Public Offering (IPO). If you’d like to work with cryptocurrency, an ICO could be your way to raise funds. If you prefer more traditional financial securities, launch an IPO, and sell your stock to secure the investments.

- Venture Capital (VC). You can create a business plan and a pitch deck to attract the attention of VC funds. If they agree to invest in your business, you will either have to give them a share or pay a fixed amount with the agreed interest.

- Bank loan. It might sound funny, but one way to raise money to build a money lending app is to take a loan. Many banks credit various business ventures, and creating a new fintech product is as good of an endeavor as any other.

Lastly, you will have to select the bank that will store your operational capital for P2P lending.

How do loan mobile apps work?

Now, it’s time to answer the next question: How do money lending apps work? The mechanics are straightforward. All users have to do is:

- Install the app.

- Register a new account or log in with their credentials.

- Select the sum they need to loan or the money they are ready to invest.

- Select the interest rate suitable for them.

- Connect their bank accounts to their lending app accounts.

Voila, all is set! iOS or Android fintech apps will automatically notify users before they deduct payments or accrue funds to their account to avoid late fees, overpayment, and other issues.

How do P2P money lending mobile apps work?

One of the biggest benefits of P2P money lending is that there are no intermediaries like loan brokers or banks. Both the lenders and the borrowers act as equal parties, so they can negotiate loan rates and repayment conditions directly with each other.

The borrower issues a loan application, and the platform approves it after a security check. Then the lender can manage the list of loan applications and approve the ones they wish. The platform gains profit as a percentage of every loan, or as a subscription fee, or in any other way, but the absence of intermediaries ensures the interest rates and terms are suitable for all users.

Money lending mobile app features

To be successful, your product has to be easy to use, like SoFi: user-friendly, with a clean UI and transparent interactions. It must work smoothly for admins, users, lenders, and borrowers.

Basic money lending app features

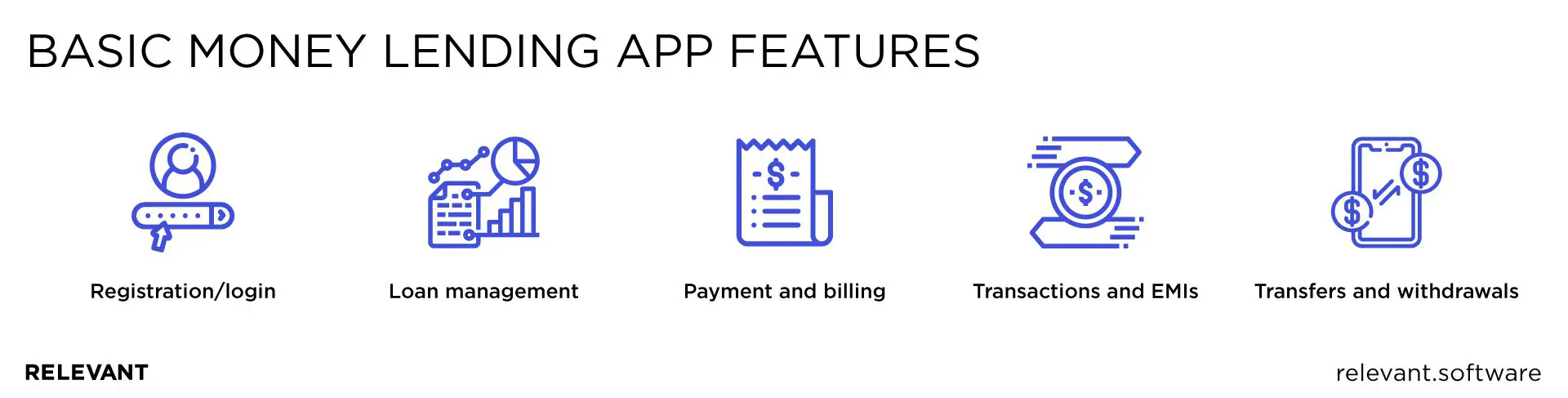

Let’s take a look at the must-have features of fintech apps.

- Registration/login. A user should be able to register and log into their account via a phone number, email, or even Facebook account. Users should also provide their contact details the platform will verify.

- Loan management. A user should be able to view the available loans, their Equated Monthly Installments (EMIs), the Goods and Services Tax (GST) value, the platform processing fees, etc. The borrowers should also be able to create their loan applications and publish them, select the estimated payback period, and communicate with lenders to discuss various aspects of the money lending process.

- Payment and billing. The loan app should store a history of all payments to provide transparency into the lending process.

- Transactions and EMIs. To pay back the loan, a borrower must pay EMIs that cover both interest and principal. Once all the EMIs are paid and the loan is returned in full, these transactions should be saved for the convenience of audit and further reference.

- Transfers and withdrawals. The money lending app should provide options to withdraw funds to a bank account or directly to the user’s banking card.

These are just several features of a loan app, but the list can go on.

Additional peer-to-peer lending app features

Chatbots, reporting, user and loan management statistics, admin actions, and many other features are essential for a smooth and convenient money lending journey for all parties.

- Reward points and ratings. Borrowers and lenders can be rewarded with points for timely fulfilling their obligations, thus rating them as reliable partners for future deals.

- Customizable reporting. The app must provide reports for all parties — how many loans are active for every user, how many EMIs are paid, how many are yet to be paid, etc.

- Chatbot. Adding a chatbot can be a good way to teach new users to master the app quickly and help them navigate through its functions.

- AI-based analytics. Admins and users can both benefit from real-time analytics. Lenders can evaluate the KYC details of potential borrowers and assess their credit history. Admins can get detailed analytics on various aspects of platform operations, using big data and AI in money lending to gain actionable insights and improve user experience.

The more advanced features you implement, the better you stand out among competitors. Determining which features are must-have and which are just nice to have is crucial for launching a successful MVP that will generate profit.

Speaking of an MVP, how much does it cost to develop a loan lending mobile app? Let’s take a closer look!

Loan application pre-development stages

To create an app like Possible Finance, you need to know the current market expectations, make a list of MVP features to meet them, and select a proven technology stack to build these features cost-efficiently and within the expected time frames.

Here are the stages you will have to go through before engineering.

Discovery

By all means, do market research first. Find out what popular apps are out there, download a few (they are usually free), analyze their features, see where they excel and where they fall short. Read the comments and pay attention to the negative ones as they might show you room for growth and a Unique Selling Proposition (USP) for your product. Gather opinions of the target audience through focus groups and questionnaires, and then form a list of app features based on this preliminary research.

Planning

Talk with your team and discuss the features you want to have implemented in the app. Work with a business analyst, team lead, and project manager to select the features most valuable to your potential users and prioritize their development within the MVP scope. This stage should end with a Scope of Work (SoW) document and a roadmap with project deliverables, cost, and time estimates.

Choosing the technology stack

Select the most appropriate tech stack for developing fintech apps. Use the tech expertise of your team and the data gathered from competitor analysis. Consider aspects like security, performance, future scalability, ease of integrations, ease of adding new features, etc.

Gather a team

Depending on the final scope and the technology stack, you may need to put together a team that consists of a team lead, UI/UX designers, front-end developers, back-end developers, iOS and Android developers, QA specialists, and a project manager.

Prototyping and MVP creation

Once the technology stack is selected, and the team is assembled, they can start prototyping to deliver a clickable and interactive prototype of your future app. When you are satisfied with its look and feel, the team can build an MVP based on the SoW document.

You don’t have to build an MVP, but we recommend doing it to release the app faster and gather user feedback sooner. This helps avoid investing in an app users don’t really need or like.

Loan lending app development cost

Depending on the scope of work, the development model, the technology stack, and the team size selected, you can roughly estimate the cost of developing a payday loan app or a P2P money lending platform. These are the cost ranges of hiring a team in various regions across the globe:

- North America: $50–$250/hour

- South America: $20–$75/hour

- Western Europe: $50–$200/hour

- Eastern Europe: $20–$100/hour

- Australia: $40–$170/hour

The quality of services varies on the location, too. While top talent is hired by US-based startups and corporations, the demand is still much higher than the supply. So, bold entrepreneurs prefer to look for loan lending app development services offshore. Most of them find that outsourcing to Eastern Europe offers the best price/quality ratio.

What development model to choose for your money lending app?

Selecting the correct development model ensures the best cost-efficiency of your app development. What will it be?

Product development

This one works best when you have the idea and the investments but lack the team to turn the concept into a working product. In the case of product development, the technology partner you choose will have to provide a full cycle of product development: from ideation to design, coding, release, and ongoing product support.

Dedicated team

Sometimes, you have enough in-house expertise to start building an app but struggle to scale fast enough or attract the specialist needed to advance the development under tight deadlines. This is why hiring a dedicated team is the best way to get instant access to the necessary talents and ensure software development and scaling go according to the approved roadmap.

We can build a loan app for you

Relevant is a technology partner with deep expertise in fintech app development. We know what technology stack to choose, what features to implement, and how to deliver an MVP on time. Here are some examples of our successful fintech cases:

- FirstHomeCoach. A real estate management platform that simplifies securing a mortgage, insuring property, and handling the legal paperwork. The product was built using React/Redux, Node.js and TypeScript, PostgreSQL and WordPress. The platform has 5,000+ active online and 1,000+ active mobile users who have more than 25,000 property purchases planned.

- Payroll. A digital solution for optimizing billing through streamlining ineffective routines. The app automatically calculates payrolls for accounting departments in companies big and small with minimal alterations. It was built using PHP, jQuery, Node.js, and MySQL. This product helps increase the reliability of accounting for companies at scale.

The bottom line

Demand for credit never really slows down. Students still pay off student loans, patients still carry medical debt, and businesses still borrow to manage cash flow. That steady demand keeps lending apps a prominent financial tool, and many startups and entrepreneurs are looking for loan lending app development services right now. Are you one of them?

Whether you need a full-cycle peer-to-peer money lending app development or simply want to expand your team quickly, Relevant can help you do that. Contact us today, and our experts will be working on your app in no time!