Boom of Embedded Finance 2020-2025: An Expert Overview

Andrew BurakCEO and Founder at Relevant Software

Andrew BurakCEO and Founder at Relevant SoftwareEmbedded finance has already become one of the most discussed terms in the fintech world. But what does it mean exactly? In short, embedded finance is when financial services are integrated into mobile apps, sites, or business processes of non-banks.

This creates a brand-new way of financial services distribution and new opportunities for tech companies to influence and improve the financial lives of businesses and consumers.

The past several years have seen financial services integrated into a great variety of software offered by non-financial services companies. And if you want to keep up with the latest trends and outperform your competitors, you should start thinking about EF solutions as well.

Relevant Software provides world-class outsourcing and fintech software development services for over 7 years. Our experienced team will help you develop and embed custom finance solutions tailored exactly to your company’s needs.

But if you are not ready to make a decision yet but want to find out more about embedded finance, keep on reading.

In this blog, you will find answers to questions such as:

- what are the benefits of embedded finance

- which industries leverage the advantages of EF

- what are the examples of EF usage

- why it’s time to invest in embedded finance solution

Embedded finance: How did we get here?

For decades, if not centuries, services like lending and payment processing were the exclusive work of banks. Because of the numerous rules and restrictions, it was practically impossible for other organizations to provide any banking services.

That was until the Open Banking movement, and its supporting regulations like PSD2, broke down the barriers. Today, any regulated entity can connect non-finance companies to banking service platforms. The result? – Embedded banking. This intersection of finance and technology brought an unparalleled shift in the financial services landscape.

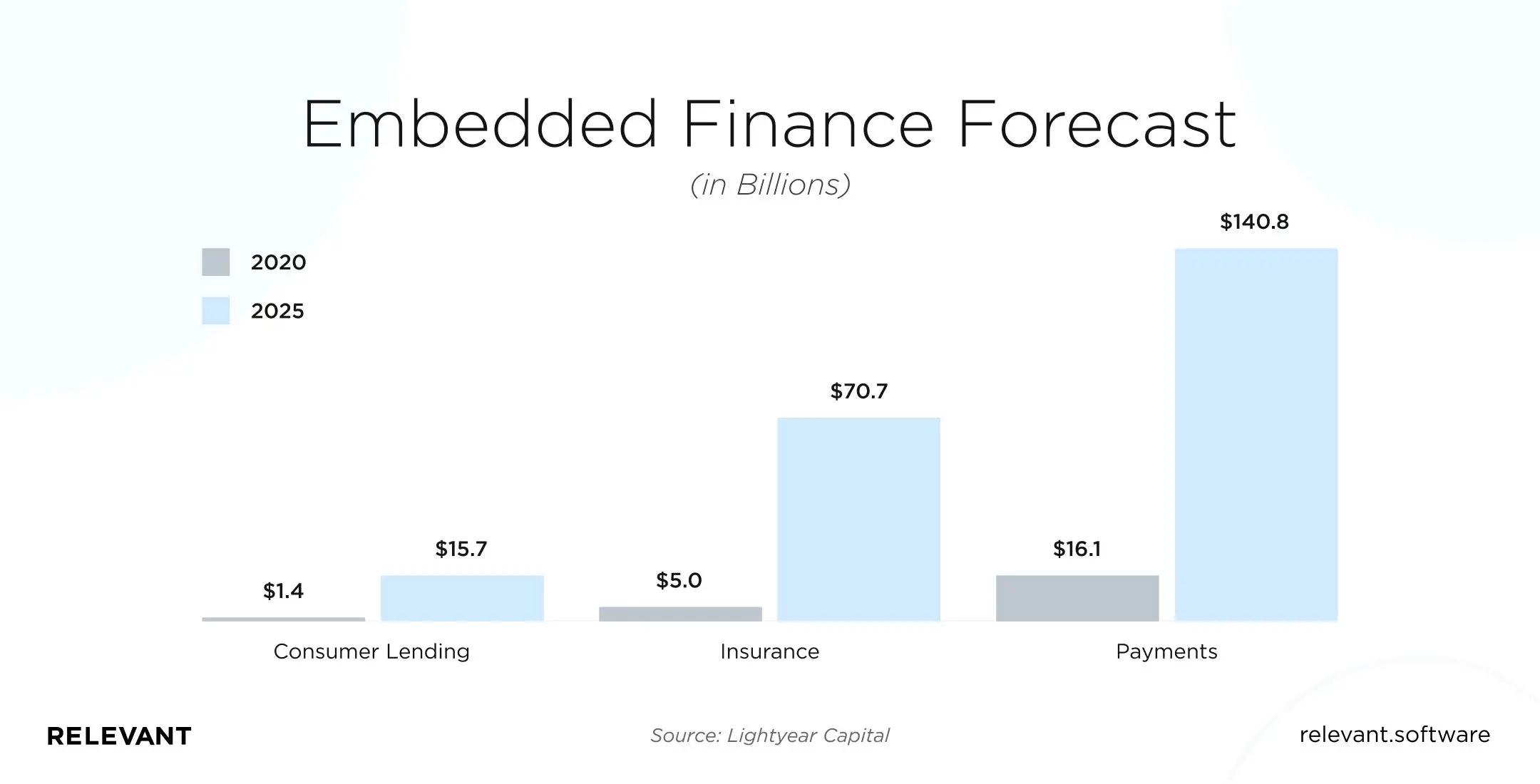

The image below from Lightyear Capital’s analysis of embedded finance best illustrates where the EF market is now and where it is headed.

The rise of fintech in finance enables non-financial companies to provide financial services to their clients, so they don’t have to visit branches. This includes embedded payments, loans, digital wallets, etc.

According to Lightyear Capital, embedded finance will generate $230 billion in revenue by 2025. As if that is not enough, it has been predicted to grow into a $7 trillion industry in 10 years.

With this in mind, more services are using embedded payments to improve user experience on their platforms.

We have seen this intersection of tech and finance embraced by taxi companies like Uber, for example. They have the payment automated into their service, thereby removing the actual paying for a service.

What drives embedded finance growth?

Embedded banking has brought so much positive change in a short space of time. This is a field that will continue to grow for the following reasons and more:

- It solves problems

Uber made use of it in making sure its drivers have on-time and consistent payments. It also helps those who don’t have bank accounts to receive their payments without waiting in long queues or dealing with paperwork. - It makes sense financially

Embedded banking creates viable opportunities for companies. A good example is how Square started as a payment processor and evolved into a point of sale company, a CRM, and an inventory management service provider. - It adds value

Embedded banking allows companies to assess customer habits and provide them with customized services. Additionally, it helps consumers by analyzing their financial habits and giving them valuable, timely recommendations.

What are embedded finance opportunities?

Embedded finance is creating plenty of opportunities both for individuals and businesses. Think of how easy you can get a loan, add a QR code payment option to your site, or provide a buy now pay later option for your clients.

With the help of embedded finance solutions, businesses can provide instant credit on their platforms. Another impressive opportunity is that of the in-demand digital mortgage service.

Finally, for those seeking to invest, embedded provides an easy-to-use platform to do so without having to leave the comfort of your home.

Well, it seems that the possibilities of embedded finance are endless. Therefore, not surprisingly, that many embedded finance startups, seeking to increase the range of embedded finance opportunities appeared in this field.

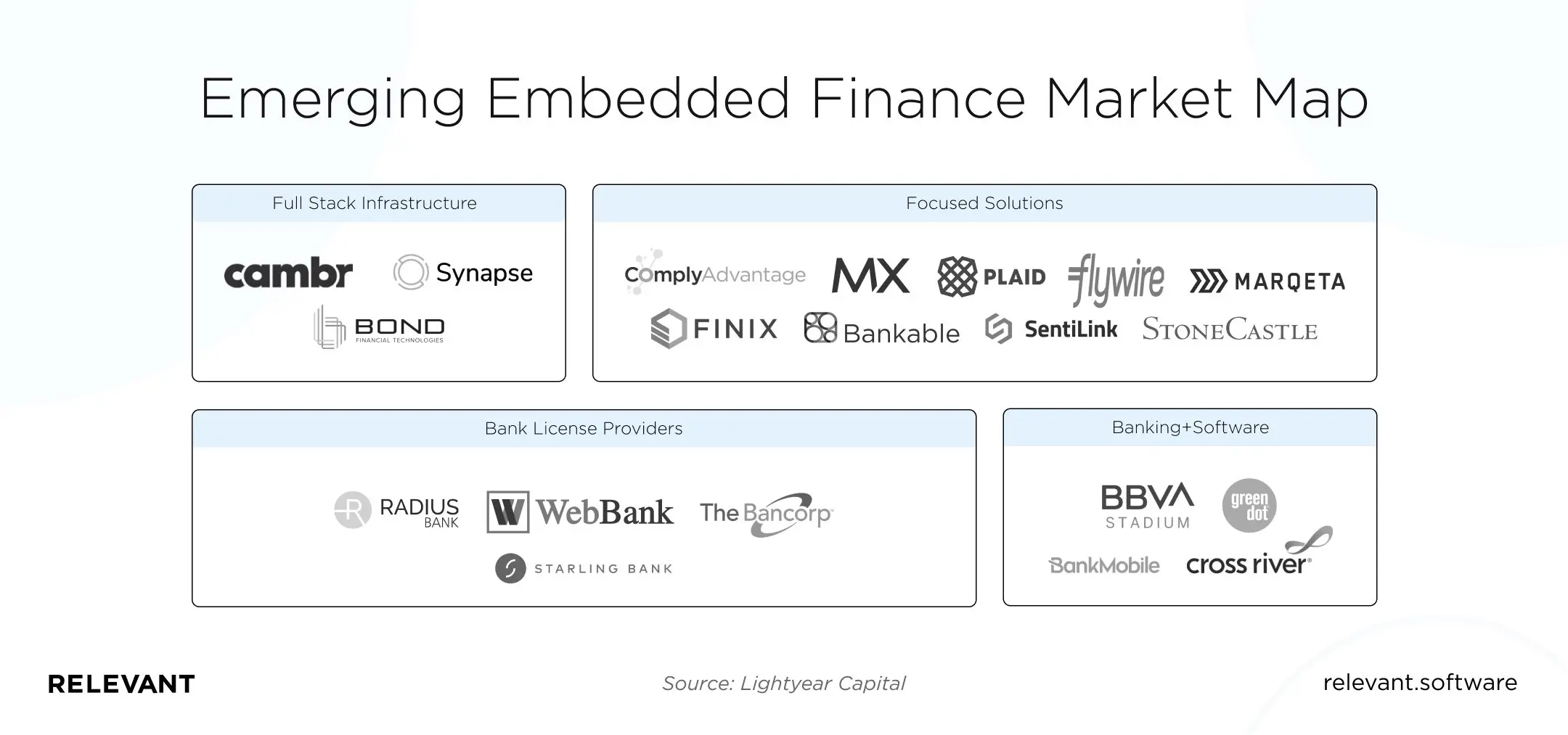

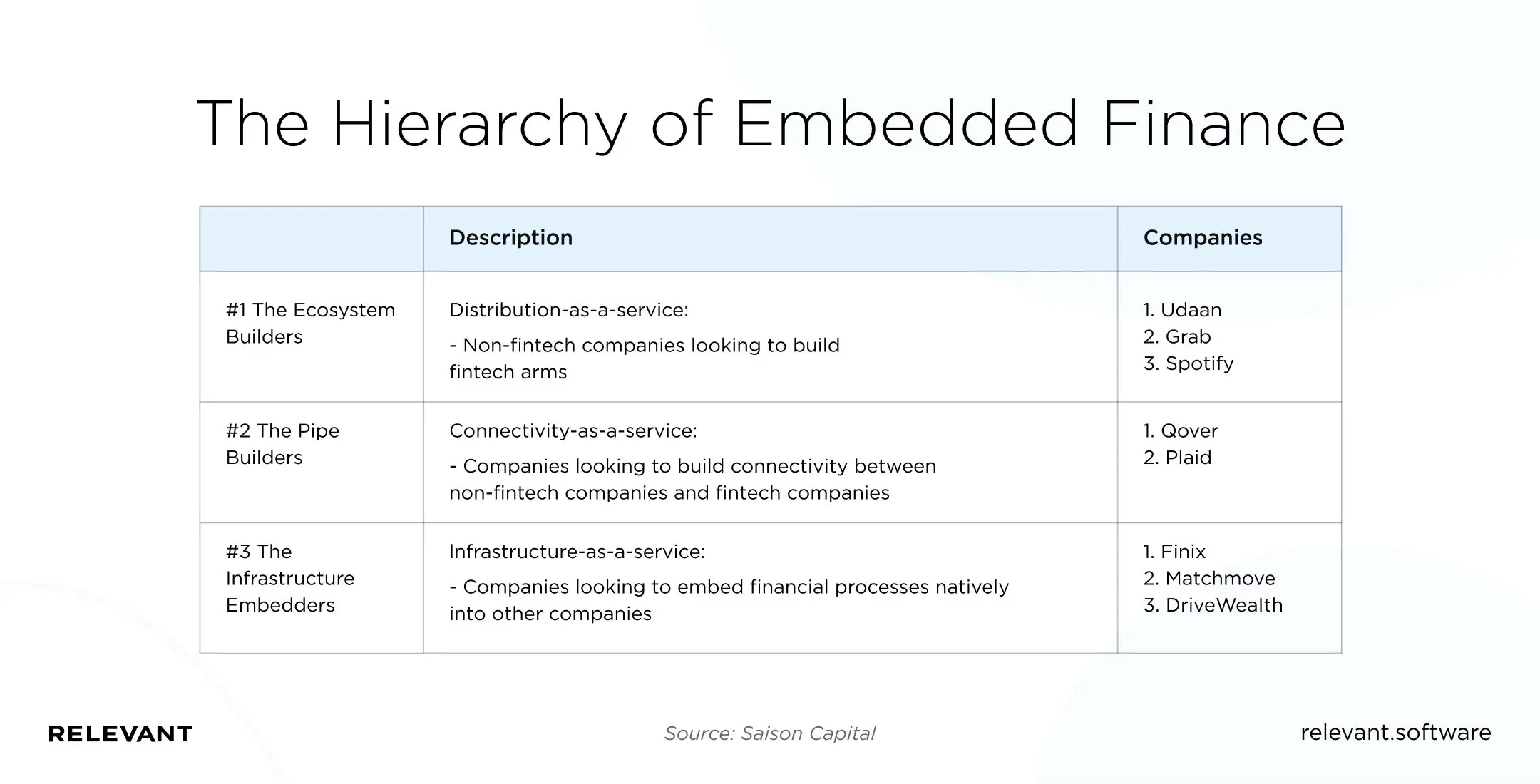

How does the embedded finance ecosystem look like?

Although EF is still an emerging concept, analysts already define at least four types of players on the market. According to Rosenblatt Securities, these are:

Full-stack solutions. This category includes end-to-end infrastructure providers that offer services like core transaction processing, banking relationships, and customer service in one package.

Focused solutions. The companies from this category offer one specific service instead of multiple services. They can help embed investing services, provide fraud detection solutions, set up payment processing infrastructure systems, etc.

Financial institutions that combine banking licenses and software. This type of organization can offer a banking license or provide the software stack for non-bank companies to embed financial services.

Pure play banking institutions. These are not direct vendors of embedded finance solutions but still help to develop the EF ecosystem. A good example of how they do that is by lending a banking license to non-financial companies that need it to accomplish their EF projects.

What are the practical examples of embedded finance?

There’s a broad range of applications of embedded finance in different industries. Which industries are these? Check out a few examples below.

- Healthcare – using an embedded finance approach in healthcare helps providers leverage the data sets they have to match patients with customized coverage. This model allows patients and hospitals to use their time and money much more efficiently.

There is still a lot of room for innovation of the embedded finance applications in the healthcare field. An important use case is one in which a patient can gain access to credit while ordering a particular service of a medical organization. - E-Commerce – during the pandemic, more people started to shop online. Many businesses started making use of embedded finance and encouraging their clients to use these services.

Services like e-wallets and instant payments for merchants are embedded banking services that serve as a viable payment gateway for most consumers.

According to a recent study, 61% of Germans would prefer eCommerce-integrated embedded financial service. According to the same survey, over 25% of respondents would be ready to open a checking account with Amazon. - Automotive industry – the automotive brands have always worked with financial institutions directly, but it seems that the times are changing. Tesla is a good example of how to leverage embedded finance to improve its customers’ experience.

Some brands allow shoppers to use sites and apps for lease payments, however, Tesla offers much more than that. For example, insurance. The company already sells car insurance in California and has ambitious plans to become “a major insurance company ” in the United States.

Another example of how embedded finance is changing the automotive industry is payments in ridesharing. With the help of embedded financial services, companies like Lyft allow customers to pay right from their apps.

What are the cases of embedded finance usage?

If you have used any of the services mentioned below, you have used an embedded banking service. Here are some practical embedded finance examples:

- Shopify. In partnership with Stripe, Shopify financial services processed upwards of $14 bn gross payments volume in the third fiscal quarter of 2020.

- Digital wallets. Amazon, Apple, Facebook, and Google are examples of large tech companies that utilize embedded finance in services like Apple Pay, Google Pay, and Facebook pay.

- Uber. Forbes states that Uber sends more than 70% of its driver payouts through Instant Pay. This is an embedded banking service they use by leveraging the debit rails of Visa and Mastercard.

Why is embedded finance important to your business?

No business should be left behind as that would be simply handing competitors your clients on a silver platter. Here is why:

- Redesigning businesses’ price chain

This can be explained by addressing the question, what is banking as a service? The COVID-19 pandemic has uncovered other ways in which businesses will communicate effectively and manage.

After adapting at an unprecedented scale and pace, many companies are forced to approach client desires in new ways, which will stand the test of time. Businesses will rethink their value chain and try to contour operations, build new revenue sources, and scale back costs.

The rise of embedded finance, also known as banking as a service (BaaS), allows businesses to avoid headaches and prices of hiring specialists who develop new services and guaranteeing they comply with regulations.

The increase of third-party BaaS suppliers means that corporations can give the monetary services capabilities that suit their distinctive necessities and not need identical investment like it would have done previously.

In addition to all this, embedded finance makes the complex process of B2B payments simpler and faster contributing to increased company productivity. - Disruption of the payroll

Embedded finance shakes things up in processes, including at the very beginning. Businesses will include this technology as an instance payroll. This would provide regular, on-demand payments of salaries.

Salary advances and early direct deposits would be possible, enabling account holders to receive paychecks in advance. This gives businesses the ability to be lenders to their employees and so generating more income. - Change in human behavior

The shift in individuals’ behavior should be of note. The pandemic meant all people had to form fashion changes. This brought a new shift in demand for online and digital services in 2020-2023. With this becoming a new norm for most, this shift will continue in 2024-2025 and beyond.

Looking ahead of time to a post-pandemic world, it is clear some trends are staying. The foremost outstanding is the progression from physical to digital.

McKinsey & Company did an analysis that suggests many will continue to make some of their purchases online. Hence, embedded finance gives businesses a chance to interact with new and existing audiences online. - The digital experience edified

Loans, credit cards, and mortgages are all services people would only get from companies that have a long history of providing such services. Things are changing, though. Today, any brand can include financial services in its business and provide clients with relevant, tailored financial merchandise.

By making use of customer data, a business can offer a much more convenient and personalized experience. Having more insights about their clients, companies are also well-positioned to assess risk. In 2024, we will see more brands take advantage of this capability. - The banks in the race

One might expect that this means the banks will become irrelevant. Several incumbents are already rising to the challenge. They are becoming enablers of entry-level business. 2024 will show the role banks will take in the evolved financial service arena.

According to Forbes, banks can take advantage of the new channels of distribution heralded by embedded finance for their products and services. Upgrading their digital banking platforms to include embedded fintech products is another option.

How to create a fintech solution fast and stress-free?

This is not just a matter of having a so-called fintech service on your platform. To be competitive and provide the best client experience, one needs their business to have a top-of-the-range fintech company be their number one solution for fintech software development.

We at Relevant are an expert technology partner with dedicated software development teams for all your fintech app needs. We are specialists in picking the perfect technology stacks and features for implementation. Others may try, but the timely delivery of an MVP is our pride.

[e-book id=”8445″]

Here are some successful fintech cases we have delivered:

- FirstHomeCoach

This is a real estate management platform with 6,000+ active users who upwards of 25,000 property purchases planned. The platform simplifies securing a mortgage, handling legal paperwork, and ensuring the property.

The product was put together using React/Redux, Node.js, and TypeScript, PostgreSQL, and WordPress. - Payroll

This app is the best companion an accounting department in a company of any size could ask for. Custom automated payroll system automatically calculates payrolls with little to no alterations. It was built using PHP, jQuery, Node.js, and MySQL.

This product has increased the reliability and efficiency of accounting for companies at scale. Impressive right? Well, now you know where to hire a software development team that delivers.

Summing up

The only direction in which business will profitably grow in 2024-2025 is embedded banking. Now is the time that will separate industry leaders and those that will ever remain in antiquity or try to follow late and always be in the shadow of their competitors.

Contact Relevant if you want to build a fintech solution that is relevant and viable or if you need some advice on how to hire a mobile app developer. We are here to help.